Stefan Dinse

On Might 4th I wrote a bullish piece on Southwestern Power (SWN) “Southwestern Power: Undervalued Herbal Fuel” arguing the inventory is price $9 according to percentage according to conservative manufacturing assumptions and the present herbal fuel calendar strip curve.

Advance a bullish thesis on a herbal fuel exploration and manufacturing (E&P) corporation like SWN and you are sure to get a couple of questions on an ETF like america Herbal Fuel Fund (NYSEARCA:UNG) that is designed to trace the cost of US-traded herbal fuel futures.

There may be good judgment to that.

In the end, the commodity pricing deck I used to price SWN contemplates a vital restoration in fuel costs into 2024 from present depressed ranges; if you are bullish fuel costs, why now not lower out the intermediary and simply purchase fuel by way of UNG?

There are primary problems with that good judgment, which I’m going to cope with in this text. Alternatively, let’s get started with this:

US Herbal Fuel Costs Are Too Low

Like any commodity markets herbal fuel costs are levered to a few basics: Provide, call for, and worth.

When herbal fuel costs are increased on the most sensible of the commodity cycle, this discourages call for and encourages better manufacturing (delivery). Sooner or later, the mix of restrained call for and rising delivery acts to carry down costs.

In a similar way, on the backside of the cycle costs are depressed. That has a tendency to inspire call for and steered manufacturers like SWN to drop drilling rigs, lower capital spending (CAPEX) to economize and make allowance manufacturing (fuel delivery) to fall.

Commodity cycles generally tend to bear for lengthy classes due, largely, to the “stickiness” of delivery. In different phrases, it takes time for emerging costs to incentive further drilling process, and for that drilling to lead to new delivery of fuel. The other could also be true – it takes a while for diminished manufacturer CAPEX to lead to a significant decline in output that is helping tighten the marketplace and put a ground below fuel costs.

Including an extra layer of granularity, what in reality issues is the marginal value of delivery and the price curve confronted by means of the marginal or swing manufacturer.

Have a look:

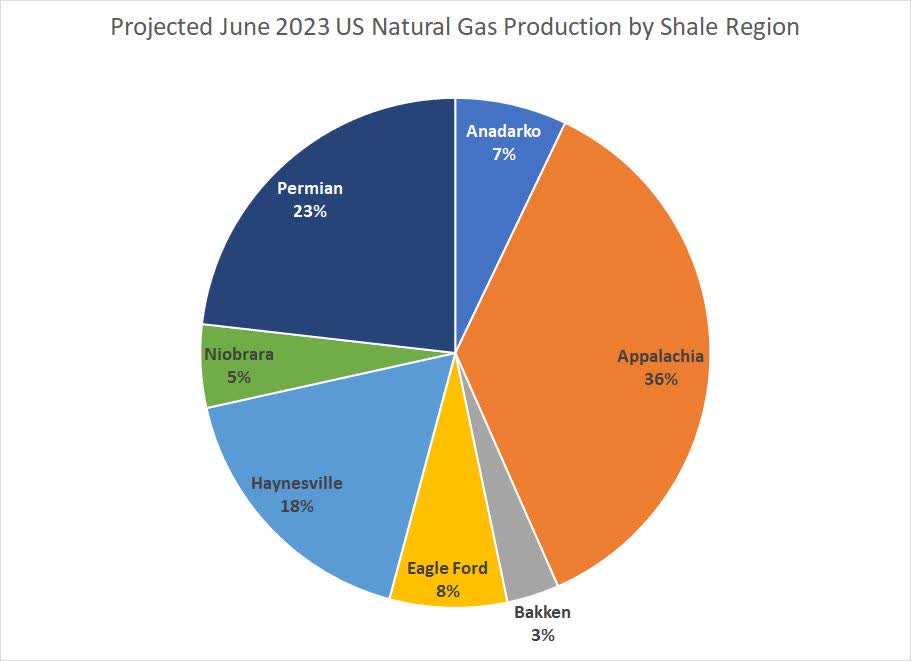

Primary US Shale fuel Areas (Power Knowledge Management)

The EIA’s per 30 days Drilling Productiveness File studies oil and fuel manufacturing and different key statistics for 7 massive US shale fields round america. For herbal fuel, those 7 shale fields produce a blended general of about 97 billion cubic ft according to day (bcf/day) of herbal fuel, in comparison to general US herbal fuel gross withdrawals of 123.1 bcf/day in February 2023, the final complete month for which the EIA supplies knowledge.

And, as you’ll see in my pie chart, 3 US shale fields account for greater than three-quarters of that shale output – the Permian Basin in Texas and New Mexico (23%), the Haynesville of Texas and Louisiana (18%) and the Marcellus of Appalachia (36%).

Maximum herbal fuel manufacturing produced within the Permian Basin is what is referred to as related fuel manufacturing. That implies this fuel is produced as a spinoff of crude manufacturing from wells which are drilled to focus on oil, now not fuel.

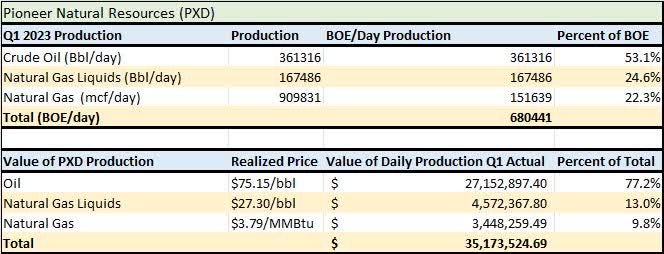

Thus, the economics of maximum wells drilled within the Permian are according to the cost of oil, now not herbal fuel. Believe the case of Pioneer Herbal Assets (PXD), a big impartial manufacturer with acreage within the Midland Basin, the japanese a part of the Permian in Texas. Within the first quarter of 2023, PXD produced 361,316 bbl/day of crude oil, 167,485 bbl/day of herbal fuel liquids (NGLS) like ethane, propane and butane and 909.83 million cubic ft according to day of herbal fuel.

Most often, oil-focused manufacturers like PXD convert their manufacturing of all calories commodities into barrels of oil equal (BOE) the use of an energy-equivalent conversion. Through conference, one barrel of blended NGLs equates to at least one barrel of oil and six,000 cubic ft of fuel (roughly 6 million BTUs of calories content material) turns into a unmarried barrel of oil equal.

Have a look:

Pioneer Assets Manufacturing Desk (Pioneer Herbal Assets Q1 2023 Income Name)

In Q1 2023, PXD’s general manufacturing was once 680,441 boe/day and on an calories equal foundation, herbal fuel accounted for 22.3% of the whole. Alternatively, that overstates the significance of herbal fuel to PXD’s industry; as you’ll see within the decrease part of this desk, herbal fuel best accounted for roughly 9.8% of the day-to-day income PXD learned in Q1 2023.

Let us take a look at this another way. In Q1 2023 PXD earned a mean worth of $3.79 for each thousand cubic ft (mcf) of herbal fuel bought. Retaining the costs of oil and NGLs unchanged at exact Q1 2023 ranges whilst decreasing the learned worth of herbal fuel to $2.00/mcf would have diminished PXD’s general revenues by means of simply 4.6%.

In a similar way, if we hiked the learned worth of herbal fuel in Q1 2023 to a hypothetical $7.58/mcf (double the true learned worth) the result’s only a 9.8% upward thrust in revenues from the Q1 2023 general. And that’s the reason with an excessive bounce in natgas costs.

My level: PXD is not going to make capital spending or operational drilling choices according to herbal fuel costs – the quantity of fuel the corporate produces is dependent upon the cost of oil.

Permian manufacturers generate various ranges of related fuel manufacturing according to the positioning in their acreage with western reaches of the play most often generating upper fuel content material. Alternatively, the primary level holds – Permian fuel manufacturing cannot be the swing basin for US herbal fuel delivery as a result of it isn’t going to modify a lot without reference to how a long way fuel costs rally or fall.

The largest supply of US fuel manufacturing is the Marcellus Shale of Appalachia, however it is also the bottom value primary box in america.

In my SWN article on Searching for Alpha previous this month, I checked out a number of US manufacturers with acreage within the Marcellus together with EQT (EQT), Chesapeake (CHK) and Southwestern (SWN). EQT is extensively (and accurately) considered as one of the vital lowest value manufacturers in Appalachia; within the corporation’s first quarter name EQT reported all-in working prices of $1.34 according to 1,000 cubic ft equal (MCFE) of fuel manufacturing.

Manufacturing prices come with rent working bills, the price of transporting fuel to marketplace and manufacturing taxes. On most sensible of that the corporate reported CAPEX, principally the price of drilling new fuel wells to offset declines from current wells, at $1.01/Mcfe.

So, that yields an all-in value for EQT in Q1 of $2.35/Mcfe, which is equal to $2.35/MMbtu by means of conference.

Equipped common fuel costs are north of $2.35 to $2.50/MMBtu over the process a 12 months, EQT can generate sure loose money drift. Or even with front-month fuel costs lately round $2.39/MMBtu, the futures worth of fuel is a long way, a long way upper than that as I defined in my SWN piece previous this month.

Consistent with Bloomberg, the cost of fuel for supply in October 2023 is $2.81/MMBtu and in December 2023 it is $3.69/MMBtu. So, Appalachia and manufacturers like EQT aren’t the “swing” providers of fuel in america both, as a result of their manufacturing sits on the low finish of the price curve and they are able to generate money drift and take care of manufacturing even at low fuel costs.

The Haynesville is the Swing Provider

As an alternative, I might argue the Haynesville has been, and stays, the important thing marginal supply of herbal fuel in america and the important thing box to look at in coming months.

That is as a result of manufacturers in Haynesville want herbal fuel costs above $3.25 to $3.50 to generate loose money drift from wells within the area.

In my April twenty sixth article “Comstock Assets: 2023 Will Be Messy,” I took an in depth have a look at pure-play Haynesville manufacturer Comstock Assets (CRK) and concluded the corporate wishes learned fuel costs of $3.19/MMBtu or upper to generate loose money drift according to their full-year 2023 steerage.

Southwestern (SWN) is a hybrid manufacturer that expects to generate about 60% of its 2023 manufacturing from Appalachia and 40% from the Haynesville. On an all-in foundation, I calculated SWN’s breakeven value at $2.84/Mcfe according to the mid-point of control value and CAPEX steerage for 2023.

Alternatively, SWN’s capital potency is way upper within the Marcellus than within the Haynesville – assuming all prices between basins are the similar aside from for CAPEX, SWN wishes round $3.26/Mcfe to generate loose money drift within the Haynesville and simply $2.35 in Appalachia.

For a time, a fuel manufacturer can refuge its money drift from commodity costs by way of hedges; alternatively, the longer herbal fuel costs stay beneath that $3.25 to $3.50/MMBtu breakeven vary, the much more likely it’s you’ll be able to see those manufacturers lower CAPEX, cut back their rig depend and cut back drilling process with the intention to cut back prices and steer clear of overspending their money drift.

In a similar way, rallies in fuel considerably above that vary — say to $4/MMBtu or upper, will generally tend to offer a powerful financial incentive for manufacturers within the Haynesville to spice up drilling process and convey extra fuel. That is as a result of they earn vital money flows at costs north of $4/MMBtu.

You’ll already see this $3.50 to $4/MMBtu worth ruin level for the Haynesville at paintings. With fuel costs smartly below that stage to this point this 12 months, CRK has diminished its rig depend within the core of its Haynesville play from 7 rigs firstly of the 12 months to six rigs with an extra rig to be launched this month.

SWN plans to function 7 to eight rigs within the Haynesville in 2023 and whole between 64 and 65 general wells within the play, a fee of kind of 16 wells according to quarter. By contrast, in This fall 2022 SWN finished 19 wells within the Haynesville.

Baker Hughes supplies rig depend knowledge for the Haynesville over the years:

Haynesville Rig Rely and Natgas costs (Baker Hughes, Bloomberg)

This chart displays the 12-Month Calendar Strip worth for NYMEX herbal fuel in orange (right-hand scale) in comparison to the Baker Hughes Haynesville Shale energetic rig depend in blue (left-hand scale). The thick horizontal black line at the chart is drawn at a fuel worth of $4/MMBtu.

The 12-month calendar strip is the common worth of herbal fuel futures for supply over the following twelve months, a extra helpful measure of costs for manufacturers slightly than the entrance month. That is as a result of manufacturers make their drilling and CAPEX choices according to anticipated longer-term fuel costs, and their hedge protection, now not the cost of fuel for supply over the following 30 days.

As you’ll see, the 12-month strip worth of herbal fuel first surged above $4/MMBtu in late-August 2021, pulled again a little into early final 12 months after which jumped once more beginning final spring.

Drilling process, measured by means of the Haynesville rig depend, answered with a lag of about 4 to five months, emerging from 45 energetic rigs in past due August 2021 to 49 by means of the top of December 2021 and over 60 by means of the top of February 2022.

We are now seeing the lagged have an effect on of fuel costs on Haynesville process as soon as once more, this time in the other way.

On the finish of final 12 months, the 12-month calendar strip for herbal fuel was once nonetheless over $4.25/MMBtu, a at ease stage for many fuel manufacturers within the Haynesville. Through the primary week of February, alternatively, the strip was once beneath $3.25 and front-month fuel futures had been beneath $2.50/MMBtu – once more, kind of 3 to 4 months later, the rig depend within the area has fallen from 70 rigs in mid-February to 64 rigs in mid-April and 57 as of final week.

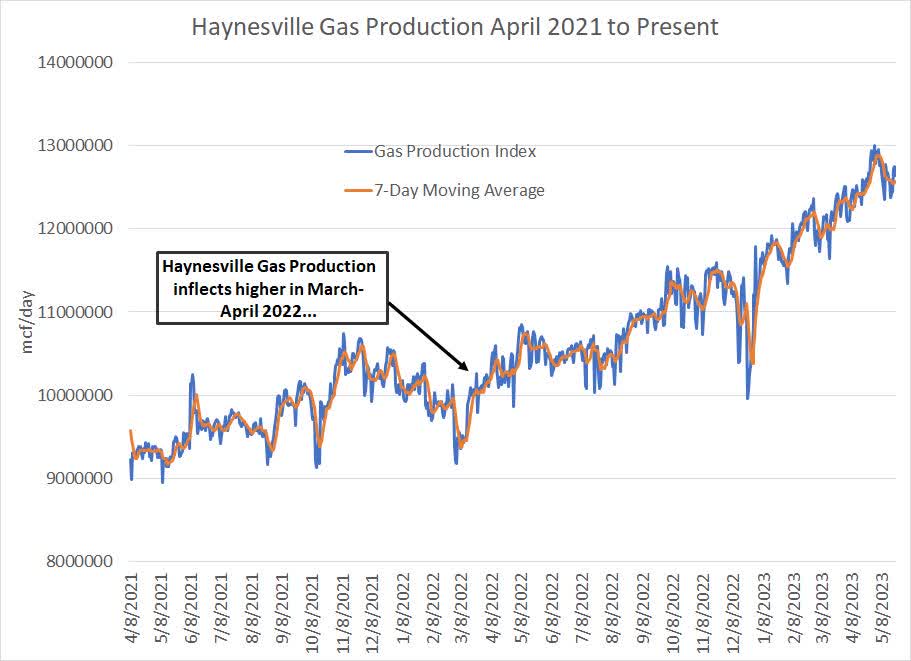

Monitoring exact fuel manufacturing from the Haynesville, no less than on a real-time foundation, is a little more tricky even though Bloomberg has a manufacturing indicator according to pipeline flows:

Haynesville Shale Estimated Manufacturing (Bloomberg)

This Haynesville manufacturing index is not at once similar to the information printed with a substantial lag by means of the Power Knowledge Management within the Drilling Productiveness File I discussed previous nevertheless it turns out to be useful directionally.

You’ll see the development of occasions right here – fuel costs rallied over $4/MMBtu in past due 2021, a degree the place drilling new wells within the Haynesville are economically horny. Then a couple of months later manufacturers answered to that worth sign by means of expanding their drilling process (a emerging Haynesville rig depend) and about 3 months later, there was once a upward thrust in Haynesville fuel manufacturing as new wells had been finished and put into manufacturing.

Those lag occasions are brought about, partially, by means of the reality manufacturers most often contract rigs for multi-month (or longer phrases), so that they drop rigs as contracts conclude slightly than adjusting drilling process on a real-time foundation. It additionally takes weeks to drill and whole a smartly and generate exact fuel manufacturing.

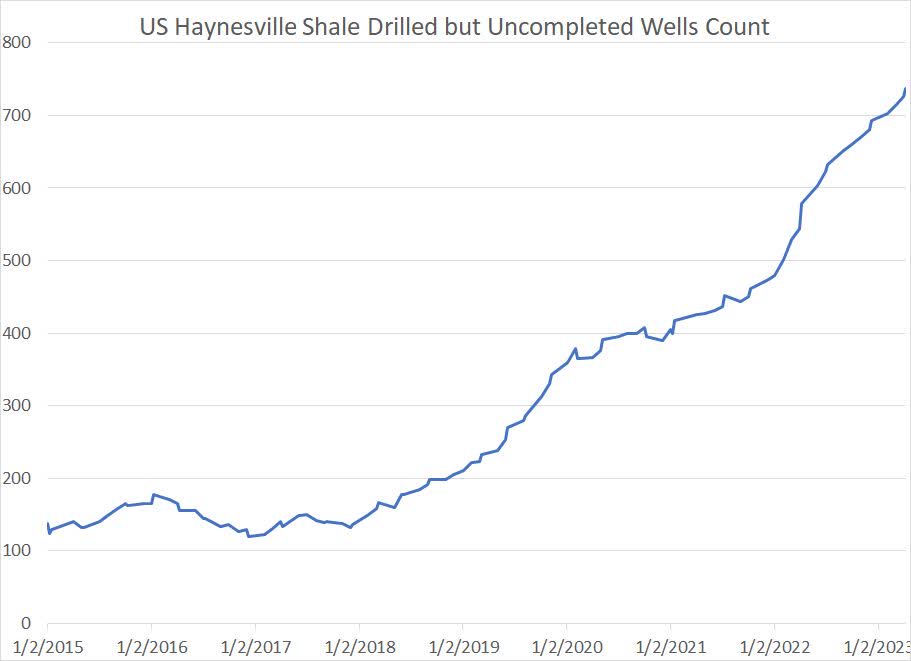

Lag occasions will range from company-to-company and cycle-to-cycle relying on a large number of things together with the dimensions of swings in commodity costs and the presence (or lack thereof) of so-called DUCs. DUCs is an acronym for drilled uncompleted wells, which can be wells which were drilled however have now not but been put into manufacturing.

Those DUCs can generate new fuel manufacturing and not using a corresponding build up within the rig depend. In terms of the Haynesville the present DUC depend is important:

DUC Rely in Haynesville Shale (Power Knowledge Management, Bloomberg)

Regardless, this, in a nutshell, is the invisible hand of markets at paintings and it is how microeconomics – particular person corporation choices on CAPEX, drilling process and smartly economics -feeds again to the massive image basics of fuel delivery and costs.

The longer fuel costs stay beneath the Haynesville money drift breakeven within the $3.50 to $4/MMBtu vary, the extra you’re going to see particular person manufacturers on this area drop rigs and lower CAPEX. In the end that may feed thru right into a flat-to-declining DUC depend and falling fuel output.

Certainly, that is already going down to a point. For instance, within the 3 months ended December 31, 2022 Southwestern Power produced 168 bcf of fuel from its Haynesville acreage, in Q1 2023 it was once 160 bcf.

The midpoint of control’s steerage for full-year 2023 fuel manufacturing throughout its acreage is 1,465 bcf, down from 1,520 for full-year 2022. SWN has indicated about 40% of general 2023 fuel manufacturing will come from the Haynesville, implying steerage of about 586 bcf from Haynesville for full-year 2023 or 146.5 bcf according to quarter.

Commodity markets be in contact to marketplace members – customers and providers of the commodity in query – by way of the language of worth. If delivery is upper than call for, then the value will in the long run drop to a degree that activates the swing providers of the commodity to scale back their output. In terms of herbal fuel, that suggests costs want to fall to a degree the place Haynesville manufacturers’ profitability is challenged.

The other is correct when delivery is insufficient to satisfy call for – costs should upward thrust a long way sufficient to incentive new manufacturing from performs like Haynesville.

At the moment, america is oversupplied with fuel and fuel garage is abundant, so costs have fallen again to the mid $2/MMBtu vary at the entrance month and $3.20 at the 12-month calendar strip. That is a degree the place best “0 value” Permian related fuel manufacturing and cheap Marcellus manufacturers in Appalachia will proceed to supply fuel whilst manufacturers within the swing area of Haynesville, reasonably upper up the price curve, get squeezed.

In the end, alternatively, the value is simply too low as a result of below extra standard delivery and insist prerequisites, the fuel marketplace wishes Haynesville volumes to steadiness. And the value had to incentive Haynesville delivery is nearer to $4/MMBtu as I simply defined.

Timing is The entirety with UNG

That each one appears like a bullish set-up for fuel costs and it’s; alternatively, if you find yourself purchasing an ETF like UNG to industry a transfer in herbal fuel, timing is the entirety.

Looking at manufacturing prices for marginal swing providers is an invaluable framework for comparing the long-term trail of costs, delivery and insist. Within the short-run, alternatively, herbal fuel costs enjoy really extensive volatility according to basics like US fuel garage and climate prerequisites.

In the end, whilst manufacturers like SWN be expecting decrease Haynesville output as we transfer thru 2023 because of a falling rig depend, that is not but obvious in charts such because the estimated Haynesville manufacturing chart I confirmed you previous. It may well be that manufacturing starts to fall meaningfully by means of past due summer time or it would take till November-December 2023 – the lag between a falling rig depend and demanding retrenchment in delivery isn’t strong over the years.

None of this is helping holders of UNG.

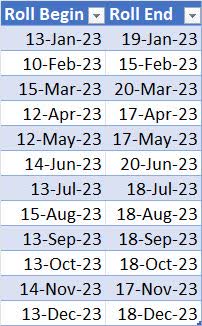

At the moment, as an example, america Herbal Fuel Fund (UNG) is invested within the July 2023 NYMEX Herbal Fuel futures, which promote for round $2.53/MMBtu. UNG rolls its publicity from one commodity futures contract to the following in step with a set time table:

Futures Roll Time table for UNG (USCF Investments)

So, as an example, the UNG ETF was once totally invested within the June 2023 Herbal fuel futures as of the top of April 2023 after which rolled publicity into the July 2023 futures between Might twelfth and Might seventeenth (final week).

Beginning on June 14th thru June 18th, UNG will promote July 2023 fuel futures and reinvest the proceeds within the August 2023 herbal fuel futures and from July thirteenth thru July 18th, UNG will go out the August 2023 contract and purchase the September contract.

Thus, the one components that may affect the cost of UNG are the ones which are anticipated to persuade the basics of herbal fuel delivery and insist between now and UNG’s subsequent scheduled roll window in mid-June.

Breakeven costs for manufacturing within the Haynesville, a a very powerful elementary individually for fuel costs over the following 12 to 18 months, are beside the point for the July 2023 contract. So too is predicted herbal fuel call for subsequent wintry weather or the massive build up in US liquefied herbal fuel (LNG) export capability from past due 2024 thru 2026 I wrote about in my piece on SWN previous this month.

None of those basics topic, as a result of they are all more likely to occur too past due to have an effect on buying and selling within the July 2023 NYMEX herbal fuel futures contract and even the August and September contracts as UNG rolls its publicity over the years.

As an alternative, I think herbal fuel costs within the brief time period will proceed to industry based totally totally on two basics – US climate prerequisites and the week-to-week swings in US herbal fuel garage knowledge.

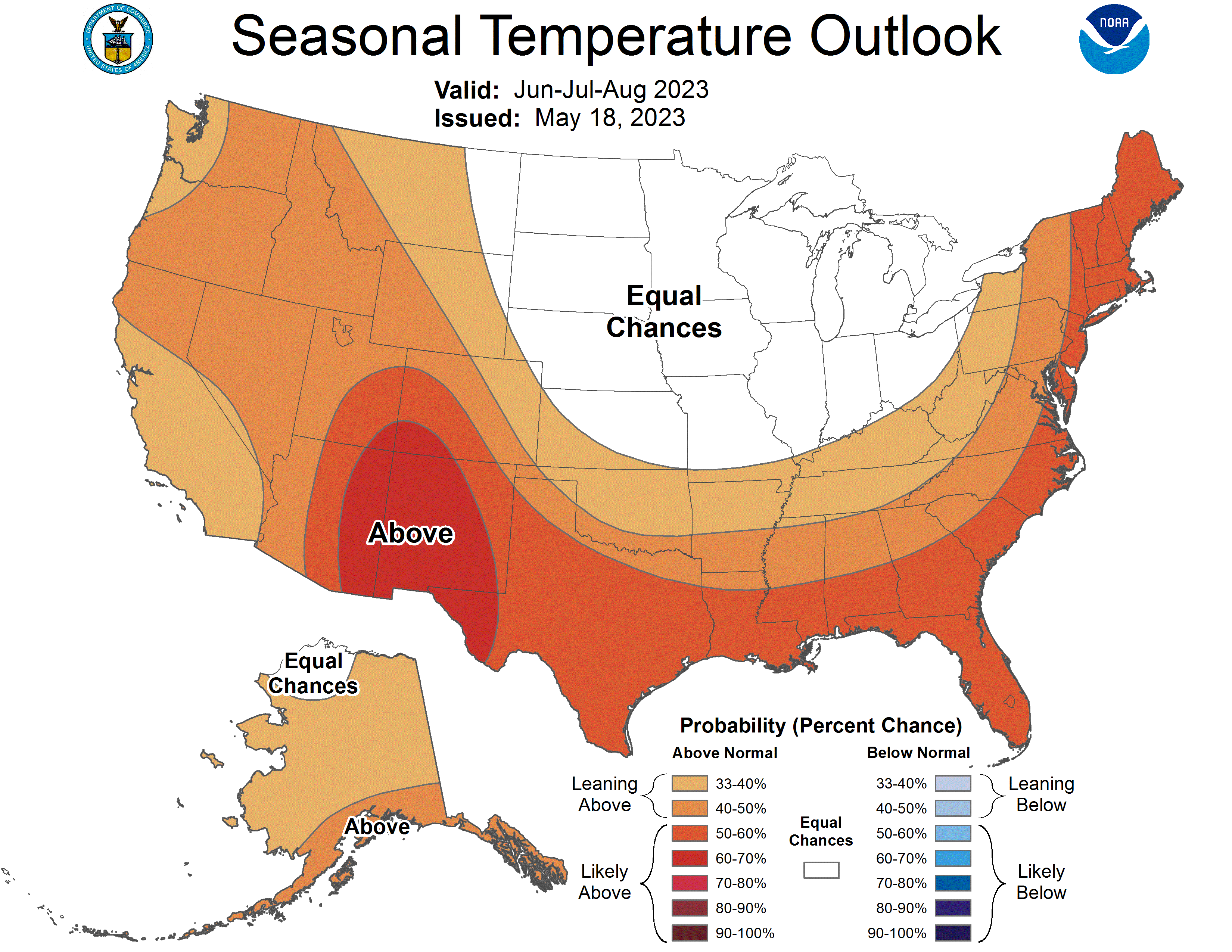

Ultimate week, as an example, the Nationwide Oceanic and Atmospheric Management (NOAA) launched its newest forecast for anticipated summer time temperatures this 12 months, summarized on this map:

NOAA Forecast for Summer season Climate (NOAA)

As you’ll see, lots of the US is predicted to look above common temperatures for the months of June, July and August 2023 and there aren’t any areas of america anticipated to look beneath common temperatures.

Above-average temperatures are projected for many inhabitants facilities alongside the Jap Seaboard, around the South and the West Coast with best the Midwest anticipated to experience extra common temperatures.

Sizzling climate way upper call for for air-con. Since electrical energy era accounts for some 35% to 40% of general US fuel call for, it is a significant momentary call for motive force for herbal fuel. July 2023 fuel futures jumped in this information, and UNG adopted swimsuit, rallying 8.4% at the day NOAA launched this forecast.

Since then, July herbal fuel futures have given again maximum of the ones knee-jerk beneficial properties due, partially, to the truth that there stays a glut of fuel in garage throughout america:

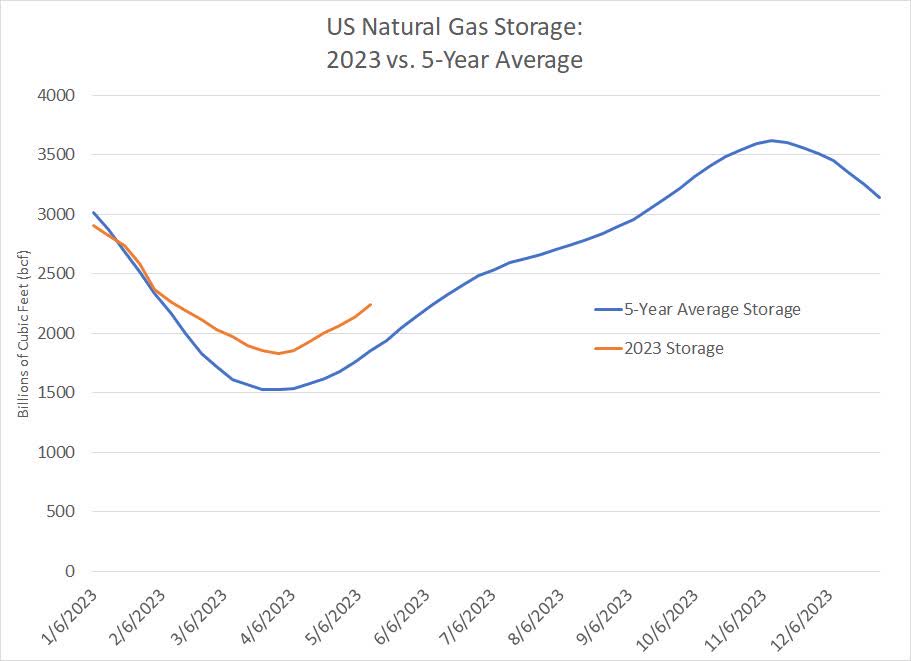

US Herbal fuel Garage and 5-Yr Reasonable (Power Knowledge Management)

This chart displays general US herbal fuel in garage every week this 12 months (orange line) in comparison to the 5-year seasonal common in blue.

As you’ll see, herbal fuel garage has began to upward thrust seasonally, a trend that most often continues in the course of the onset of wintry weather heating call for in November. At the once a year lows this 12 months, the whole quantity of fuel in garage throughout america was once round 300 bcf above the 5-year seasonal common.

As of the newest EIA garage document for Might twelfth, fuel garage was once about 380 bcf above that very same five-year common. That is numerous extra herbal fuel in garage and it will take some very popular summer time climate to near the distance with the 5-year common.

For instance, NOAA makes use of cooling level days (CDDs) to measure common temperatures throughout america, the place the upper the CDD depend, the warmer the elements. In July 2021 the whole US population-weighted CDDs depend got here in at 335 and for July 2022 it was once 365, that means cooling call for will have to were upper final July than in July 2021.

In July 2021, america fed on about 1.235 trillion cubic ft of herbal fuel (39.85 bcf/day) in electrical energy crops and in July 2022 america fed on 1.40 tcf (45.2 bcf/day).

That is a distinction of kind of 5.35 bcf/day due (partially) to better summer time cooling call for final July in comparison to 2021. Alternatively, it will take greater than two months of such increased cooling call for to erode the present 380 bcf of extra garage.

And that assumes all different components are equivalent, which is not the case. For instance, final summer time the cumulative impact of a years-long drought negatively impacted California’s hydroelectric energy output and compelled the state to depend extra closely on fuel to generate energy. By contrast, this 12 months’s historical rainfall totals and larger-than-average snowpack are anticipated to result in greater hydro output, decreasing fuel call for even in a sizzling summer time relative to final 12 months.

Base line: It’ll take greater than 3 months of sizzling climate to normalize US herbal fuel garage ranges. Much more likely it is going to require decrease fuel manufacturing over the years as I famous previous and, in all probability, a mean to cooler-than-average wintry weather in america in 2022-23. In spite of emerging call for for herbal fuel from electrical energy turbines within the heat summer time months, wintry weather heating continues to be the season of top call for for US fuel.

So, forecasting the momentary trail of UNG calls for tracking the interaction of US climate prerequisites in early summer time and the most likely marketplace have an effect on given the headwind of still-elevated garage ranges.

To be frank, my conviction in regards to the near-term outlook for fuel costs is low.

Normally, I see a ground for herbal fuel close to contemporary lows within the $2.00 to $2.25/MMBtu vary. As I simply defined, sustained costs beneath that stage are too low to toughen manufacturing even from The us’s prolific Marcellus Shale area. Additionally, whilst fuel garage is increased, it is smartly beneath the 5-year seasonal highs whilst LNG exports and exports by way of pipeline to Mexico stay sure drivers.

It is conceivable those depressed ranges may well be retested if summer time climate will get off to a fab get started or weekly garage ranges display garage construction at a quicker than standard tempo.

At the different facet, I see a rally above $3.00 to $3.25/MMBtu as not likely close to time period. A rally above that stage would start to spark issues about renewed drilling from US herbal fuel manufacturers or, at a minimal, solid doubt on a tailwind for fuel costs from the lagged have an effect on of new CAPEX cutbacks. And, with garage nonetheless smartly above standard, a rally to above backside finish of the Haynesville “breakeven” vary is unjustified.

If the summer time will get off to a heat get started or we begin to see indicators of falling US fuel manufacturing from areas just like the Haynesville, then I will see this $3 to $3.25/MMBtu area in play.

In abstract, over the following two months I see volatility in fuel costs on this wide selection with in all probability a little extra bias to upside than drawback possibility.

Sadly, it is a conviction within the momentary outlook that is required to tell a call to shop for or promote UNG- the trail of the ETF is fully dependent at the trail of July Natgas futures till the center of June adopted by means of August 2023 futures till the center of July.

By contrast, my conviction within the intermediate to longer-term outlook for fuel is upper for the explanations I defined previous and in my bullish piece on SWN previous this month.

Merely put, long term, costs will want to upward thrust above the money drift breakeven for the Haynesville within the $3.50 to $4.00/MMBtu vary to stop a persevered decline in US herbal fuel manufacturing and meet rising call for for fuel to satisfy call for for LNG exports within the 2024 to 2026 vary.

Alternatively, those intermediate to longer-term fuel call for and provide basics are beside the point to the trail of UNG over the following couple of months.

To make issues worse:

Purchasing and Protecting UNG Can Be Dear

The remaining low for front-month herbal fuel futures this 12 months was once March 29, 2023 when the cost of front-month herbal fuel futures settled at $1.991/MMBtu.

On the time, the entrance month for fuel was once the April 2023 futures; March twenty ninth was once the final day of buying and selling for that contract and maximum futures marketplace process had already shifted to the Might 2023 contract. UNG rolled out of the April 2023 fuel contract and acquired the Might 2023 contract at the 4 buying and selling days from March 15 to March 20, 2023, so on the low water mark for fuel this 12 months, UNG wasn’t in that April futures contract.

Thus, an investor buying UNG on the finish of March, was once now not purchasing herbal fuel at below $2/MMBtu, they had been purchasing an ETF that owned the Might 2023 contract, which closed at $2.184/MMBtu on March twenty ninth, a worth that was once 9.1% upper than the front-month futures.

On Friday Might nineteenth, front-month herbal fuel costs (the June 2023 contract) closed at $2.589 and the July 2023 futures owned by means of UNG closed at $2.71/MMBtu. So, to start with blush, it would appear herbal fuel costs rose considerably from March twenty ninth to Might nineteenth of this 12 months. In accordance with the entrance month futures, the value was once up about 30% and, according to the particular contract owned by means of UNG on March twenty ninth vs. Might nineteenth, the value was once up about 24.1%.

Alternatively, the cost of UNG closed on March twenty ninth at $6.90 and on Might nineteenth at $7.46, a rally of simply 8.1%.

The primary explanation why for this seeming discrepancy pertains to the method of rolling fuel futures in a marketplace in contango.

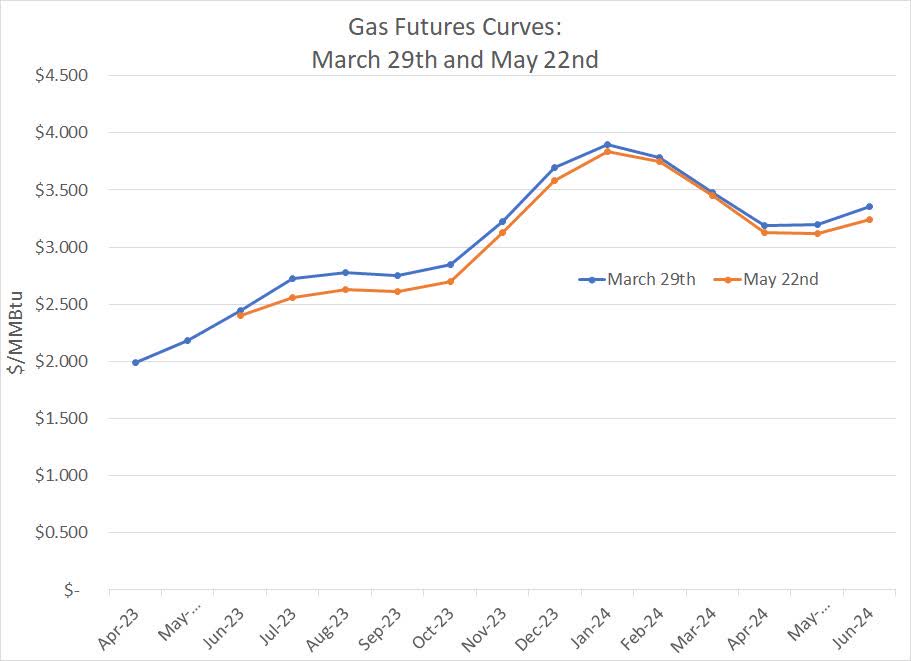

Let me provide an explanation for with this chart:

US Herbal Fuel Curve (Bloomberg)

This chart displays the herbal fuel futures curves on two dates – Might twenty second (orange) and March twenty ninth (blue). Observe that for the reason that April and Might futures contracts have already expired, I didn’t come with Might twenty second pricing for the April and Might contracts.

Two issues to notice.

First, whilst the entrance month worth of herbal fuel was once decrease on March twenty ninth, the curve lately is reasonably not up to it was once on March twenty ninth. In different phrases, the front-month on March twenty ninth was once April buying and selling at $1.991 and lately it is June futures at $2.403.

Alternatively, on March twenty ninth the August 2023 futures traded at about $2.45/MMBtu in comparison to nearer to $2.40/MMBtu lately.

2nd, each curves slope upwards in the course of the February 2024 futures contract -the worth of fuel for supply in long term months is upper than the spot worth or the front-month worth of fuel futures. That is referred to as contango.

There are a couple of causes for contango within the fuel futures marketplace lately and on March twenty ninth. For something, storing fuel prices cash, so if you wish to retailer fuel for supply in August, as an example, the price of August fuel futures will have to be upper than the spot (instant supply) to mirror that value.

2nd, call for for fuel rises in midsummer because of cooling call for, which has a tendency to tighten the fuel supply-demand steadiness. Thus, all issues equivalent, costs usually are upper in July-August in comparison to the April to June shoulder season. In the end, this “shoulder season” represents the length after US heating call for winds down and ahead of cooling call for alternatives up.

So, costs generally tend to upward thrust from spring into summer time and from fall thru wintry weather because of those seasonal call for norms. One of the vital upward slope represents genuine garage prices and a few displays marketplace expectancies for tighter call for this summer time.

This contango, and the want to roll from one contract to the following every month, represents a significant headwind for UNG.

For instance, again on March twenty ninth UNG held the Might 2023 herbal fuel futures then buying and selling at $2.184/MMBtu. When it got here time for the primary day of UNG’s scheduled 4-day roll out of the Might fuel futures and into the June contract April 12-17, 2023 the Might futures had been buying and selling reasonably upper round $2.25/MMBtu and the June futures had been buying and selling round $2.30/MMBtu.

Ultimate week when it got here time for UNG to begin roll out of the June 2023 futures and into July, the June contract had fallen reasonably to about $2.27/MMBtu and July 2023 futures had been at $2.44/MMBtu.

Thus, despite the fact that the front-month worth fuel futures seems to have risen considerably from the top of March thru get started of UNG’s Might twelfth thru Might seventeenth roll length, the cost of the contracts UNG in truth owned is best flat to reasonably upper over this period of time.

Additional, as I stated previous, the fuel futures curve is in contango, so the cost of fuel for long term supply is upper than the spot or entrance month. A few of this displays garage prices and a few expectancies for tightening basics. As time passes, alternatively, if there is not any trade in prevailing basics of delivery and insist for fuel, there is a tendency for the cost of futures to progressively fall extra in step with the present spot worth.

There is no doubt a surge in call for or a delivery surprise may crush this impact; alternatively, although the value declines by means of 0.5% to at least one% every month to mirror the erosion of the garage value baked into the futures curve, that may upload as much as a vital efficiency hit over the process longer keeping classes.

Promote UNG and Purchase High quality Fuel Manufacturers

Briefly, I am bullish herbal fuel over the intermediate to long-term. The present worth of fuel is simply too low to incentive new delivery from the Haynesville Shale, a key supply of “swing” fuel delivery.

As well as, long term, I be expecting call for for LNG cargos from america will spice up US fuel costs considerably beginning in past due 2024.

Certainly, america herbal fuel futures curve already displays many of those doable sure tendencies – the cost of herbal fuel for supply in 2024 and 2025 is considerably upper than the present worth.

Within the momentary the outlook is murkier and depends on US temperatures in June and July and expectancies for cooling call for because the summer time progresses. That is an issue for UNG for the reason that worth of the ETF is based totally only on its publicity to momentary fuel futures contracts.

Additional, because of contango within the futures curve thru early subsequent 12 months, there may be the possibility of a pernicious erosion within the worth of UNG due only to the passage of time and UNG’s pre-set time table for rolling from one contract to the following.

In the meantime, purchasing a top quality manufacturer avoids most of the drawbacks of UNG whilst giving the investor publicity to the sure longer-term tale for herbal fuel. As I defined in my SWN piece, manufacturers hedge anticipated fuel manufacturing months upfront, that means that many manufacturers have restricted publicity to near-term depressed fuel futures costs. Long term, fuel manufacturers will take pleasure in upper learned costs.

Certainly, it is a genuine, now not only a hypothetical difference – from the March twenty ninth low water mark for front-month fuel futures costs this 12 months thru Might twenty second UNG is up simply 1.45% in comparison to a 7.93% rally for SWN and a whopping 15.99% for Marcellus fuel manufacturer EQT discussed previous.