peterschreiber.media/ iStock through Getty Images

Given That I blogged about the jewelry expert Dazzling Earth ( NASDAQ: BRLT) in October in 2015, its share cost is up by 12%. I had actually provided it a Hold score at the time, however even then it appeared that the stock was at the cusp of a possible turn-around.

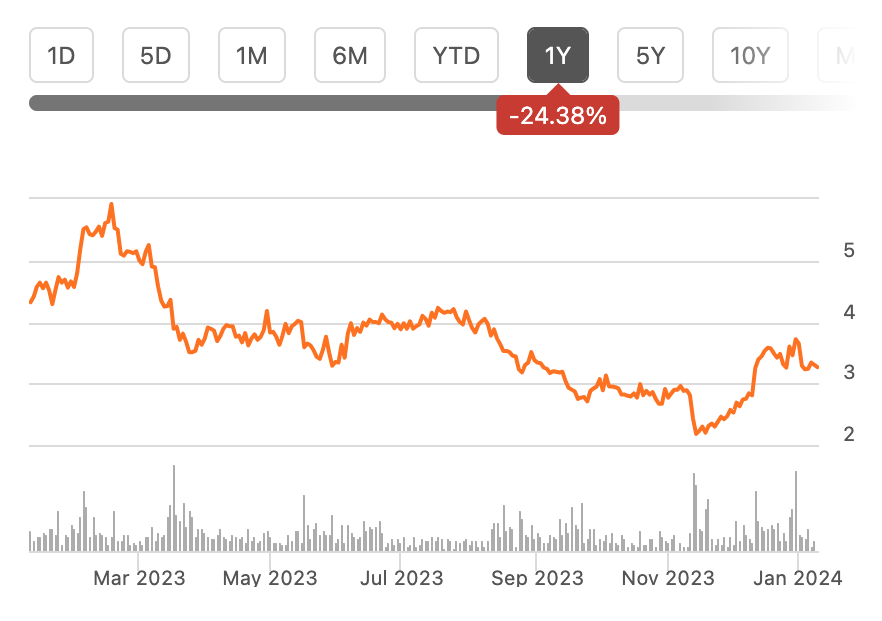

Cost Chart ( Source: Looking For Alpha)

The turn-around was contingent on a sales development uptick based upon 2 aspects. Initially, the fairly weak base of the 2nd half of the year (H2 2022) might naturally lead to greater development. Next, the joyful season in the last quarter (Q4 2023) held specific possible considering that the business had actually purchased brand-new shops and collections throughout the year. Dazzling Earth had actually likewise updated its adjusted EBITDA target, which was favorable for its price-to-earnings (P/E) ratio if it emerged.

Why did the cost increase?

As it occurs, enhanced sales development ended up being noticeable in Q3 2023, bring up the numbers for the very first 9 months of the year (9m 2023). Probably on account of softening inflation, it likewise saw an uptick in gross margin. No faster did the business launch its revenues in November, that the stock cost began inching up. Here are the crucial highlights of the revenues report:

- Net sales grew by 2.5% in Q3 2023 and brought up the development for the very first 9 months (9m 2023) to 0.6% after sales contracted by 0.5% in H1 2023.

- The order volume likewise grew by 16.7% in Q3 2023 and the boost was 19.2% for 9m 2023, up from 15.9% for H1 2023.

- The adjusted EBITDA margin can be found in at 6.4%, preserving the level from H1 2023. This is greater than the 5.7% forecasted for 2023 at the midpoint of the earlier assistance variety.

- The gross margin leapt up to 58.5% in Q3 2023 (Q3 2022: 54.7%), leading to a 57.1% margin for 9m 2023, which is a boost of 440 basis points from the very same time in 2015.

Dazzling Earth’s share bought program of $20 million, revealed in December, might likewise have actually played some part in sustaining greater cost levels. I would not worry this element excessive, however, considering that the proposed repurchase is just around 6.2% of the business’s present market capitalization and will be performed over the next 2 years. It could, nevertheless, make a limited distinction to the share cost.

Combined potential customers for the rest of 2023

In spite of the favorable patterns in Q3 2023, the course ahead for the business isn’t completely clear even now, thinking about that in the most recent revenues upgrade, Dazzling Earth reduced its net sales and changed EBITDA projection.

It now anticipates net sales to come in the series of $444-450 million, compared to the earlier projection of $460-490 million. At the midpoint, this is a 5.9% projection downgrade. While the business will handle to see a 1.6% development, it’s still a considerable decrease from the 15.7% boost seen in 2022.

The adjusted EBITDA is now anticipated to be in the series of $22-24 million, compared to the earlier forecast of $22-35 million. At the midpoint, this is a downgrade of 19.3%. Needless to state, this represents a far larger drop in the revenue step of 41% compared to a 27% decrease seen previously. The adjusted EBITDA margin is now anticipated to be 5.1% compared to 6% earlier, both of which are a decrease from the 8.9% in 2022.

While the adjusted EBITDA margin is anticipated to be remarkably little at 1.7% in Q4 2023, it isn’t all bad. The net sales development price quote is 4.5%, which will make it Dazzling Earth’s finest quarter for development in 2023.

Projection for 2024 and beyond

Experts anticipate a more uptick in profits development to 5.1% in 2024 and likewise anticipate a sharp healing in the revenues per share [EPS] by 39.4%. For viewpoint, the GAAP watered down EPS has actually decreased by 80% for 9m 2023 while the adjusted diluted EPS has actually decreased by 27.8% throughout this time.

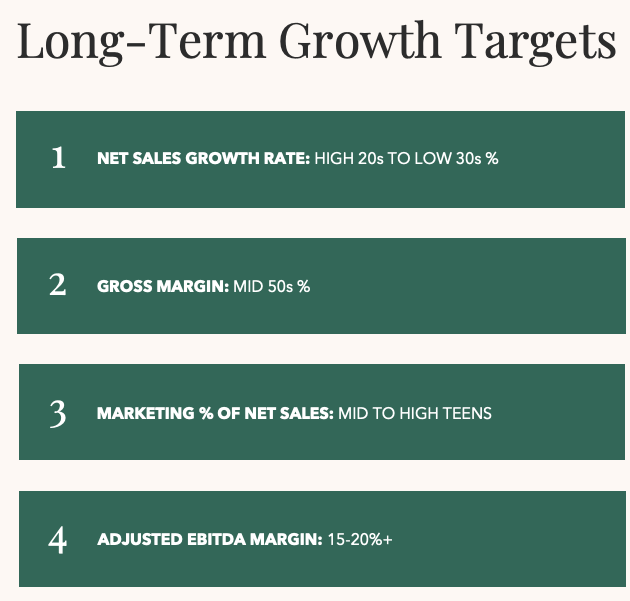

The business itself has enthusiastic long-lasting targets also, both in regards to profits and changed EBITDA (see chart listed below). Favorable as they are, it’s uncertain whether it can attain these targets currently.

Long Term Targets ( Source: Dazzling Earth)

Development driven by growth

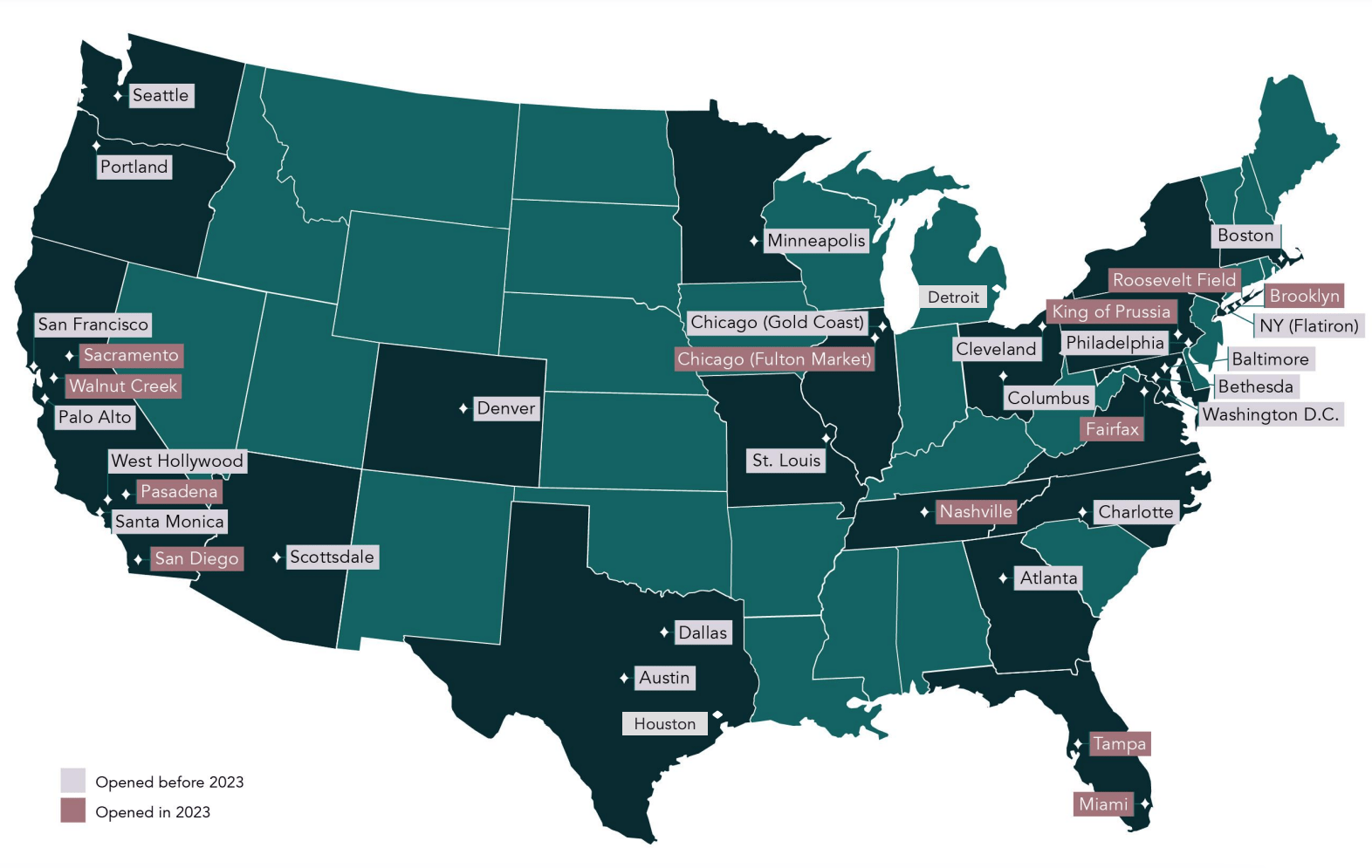

Possibly underpinning the enhanced expectations for the business are its shop openings. In Q3 2023 alone, it opened 5 brand-new display rooms and as much as 9m 2023, it had actually currently opened 37 brand-new display rooms, surpassing its full-year target. The business has likewise stated that a few of these are “yielding strong incremental development”.

Display Room Openings In 9m 2023 ( Source: Dazzling Earth)

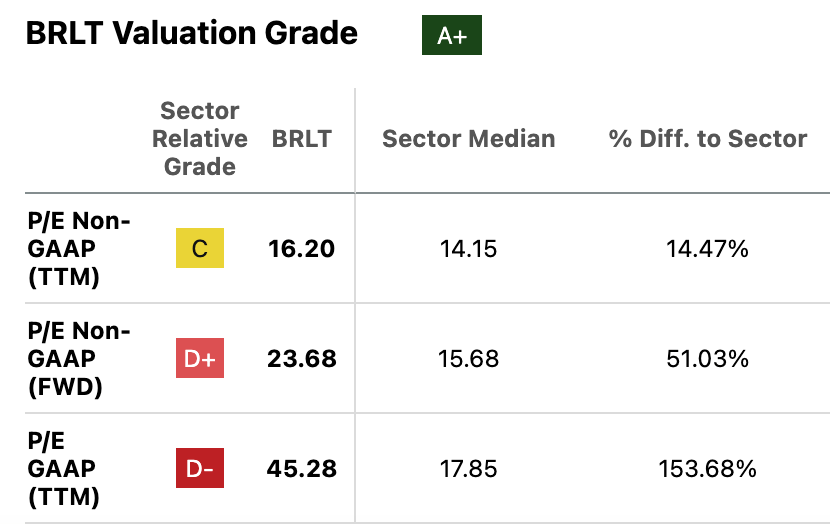

Market multiples are high

The favorable potential customers for 2024 lead to a forward non-GAAP P/E ratio of 17x, which is still greater than that for the customer discretionary sector at 15.7 x, just like the remainder of the P/E ratios (see table listed below). Significantly, the non-GAAP forward P/E is likewise much greater than the 9.75 x ratio for its instant peer Signet Jewelers ( SIG) together with the other multiples also.

Source: Looking For Alpha

What next?

With this as the background, it is difficult to support a Buy score for Dazzling Earth, even with the current cost increase. Sure, there are indications of enhancement. Its profits development has actually turned favorable, and Q4 2023 will likely be its finest quarter in the year. The sales projection for 2024 is favorable too.

However the revenues photo is desiring. It has actually seen a huge decrease in revenues this year. While this is reasonable passing its financial investments in shop openings this year, the current downgrade in adjusted EBITDA expectations is frustrating. It’s motivating, though, that experts anticipate an uptick in revenues in 2024, making its forward P/E fairly more appealing.

In the meantime, nevertheless, I want to wait on the business’s outlook for the year when it launches its full-year 2023 lead to March. These can assist identify if Dazzling Earth can undoubtedly see an excellent 2024. By that time, it’s likewise possible that the cost will remedy from its present highs to produce better-placed market multiples. I’m maintaining a Hold score.