Chris Hayward

After the bell in 2015 Thursday, we got 4th quarter outcomes from chip huge Intel ( NASDAQ: INTC). Like numerous names in the semiconductor area, Intel has actually seen its shares rise in current months as financiers anticipate remarkable income increases originating from the coming expert system (” AI”) transformation increasing chip sales. Sadly, Intel’s present quarter assistance left a lot to be wanted, stopping the remarkable rally rather all of a sudden.

Up into early 2022, Intel was producing more than $18 billion in income each quarter. Nevertheless, provided some financial softness and the business falling back rivals, the leading line plunged over the next couple of quarters, dropping listed below $12 billion in Q1 2023. While the business has actually been speaking about going back to the magnificence days with time, this was not anticipated to be a “V” formed income healing where things snap back simply as fast.

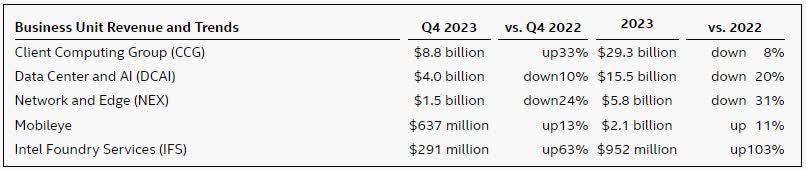

Intel has actually definitely made some development, as Q4 2023 profits can be found in at more than $15.4 billion. That figure was up 10% over the previous year duration, and it beat street price quotes by more than $200 million. The business beat expert income expectations in each quarter in 2015, reversing a variety of misses out on seen in the previous year. The development was led by the Customer Computing Group, which as management gone over on the call, was because of stabilizing stocks and strength in the video gaming and business sections.

Intel Sector Income ( Q4 2023 Revenues Report)

The big drop in profits likewise had a remarkable influence on margins, in fact sending out the business to an adjusted loss in Q1 2023. Management has actually worked to repair that issue, and the income rebound has actually definitely assisted. Non-GAAP gross margins in Q4 2023 were up 5 portion points year over year, while main business expenses were down 11%. This resulted in a rise in the operating margin from 4.3% to 16.7%, in addition to a remarkable rebound in Non-GAAP profits per share. A 54 cent adjusted earnings was reported in Q4, and while still well off levels from a couple of years back, the outcome did beat the street by almost a cent.

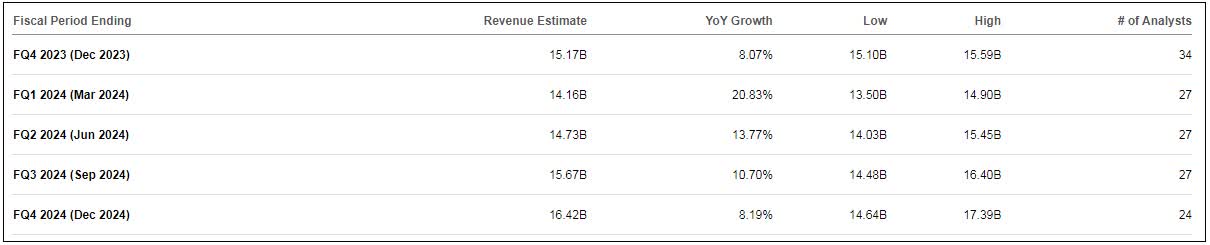

Sadly, Intel’s development has actually struck a significant speed bump at the minute. Management is requiring very first quarter of 2024 income to be in a variety of $12.2 billion to $13.2 billion. The leading end of that assistance was almost $1 billion listed below the street’s typical quote of $14.16 billion. Management stated that outcomes are being available in at the lower end of their seasonality variety for the core companies, and likewise spoke about some left companies offering income headwinds. Furthermore, there are material stock corrections at a few of the smaller sized sections like Mobileye and PSG. As seen listed below, Q1 was expected to have the greatest income development rate of 2024, however that the midpoint, just 8.4% of development is anticipated. It might not be a surprise then that adjusted profits assistance of 13 cents was simply a portion of the 32 cents that experts were searching for.

Intel Income Price Quotes ( Looking For Alpha)

Maybe what stressed me most was management’s commentary on where things are presently. It appeared like there was an event of things simply not being as bad as they utilized to be. There was a reiteration of assistance for the Data Center sector to reveal development this year, however that’s inadequate development for a lot of financiers. Rivals like Nvidia ( NVDA) are revealing enormous development in this crucial location, revealing more year over year dollar development than Intel is reporting in overall for this service sector.

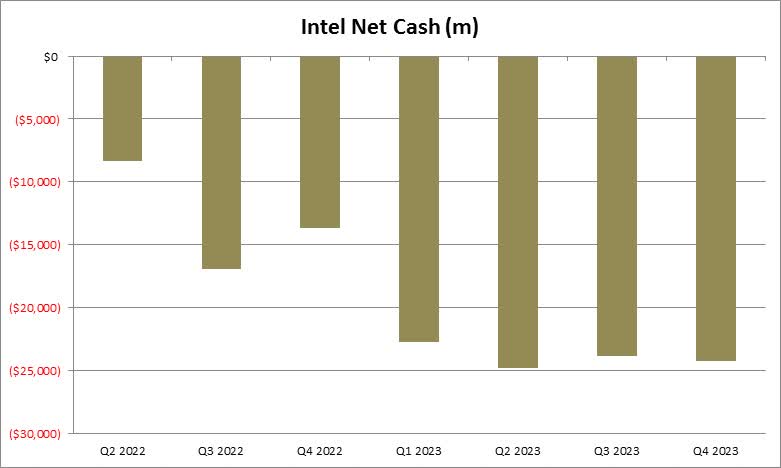

Intel ended up Friday trading at almost 33 times the street’s anticipated profits for this year. That figure was well listed below the 45 times that rival Advanced Micro Gadget ( AMD) was opting for, however a bit above what Nvidia brought at 30 times. Intel is not anticipated to reveal as much income development as AMD or Nvidia for the present year, and it likewise has a weaker balance sheet presently than both of its rivals. Intel reported adjusted money burn of almost $12 billion for the complete year in 2023, completing the year with about $25 billion of money and short-term financial investments however likewise more than $49 billion in overall financial obligation. The previous 18 months have actually been difficult as the chart listed below programs.

Intel Internet Money ( Business Revenues Reports)

The business is wishing to be approximately recover cost in regards to adjusted capital this year, indicating another year where the balance sheet lags while rivals substantially enhance theirs. With Intel likewise paying a couple of billion in a dividend to investors, simply recovering cost on capital implies a decrease in net money (or a boost in net financial obligation). This might suggest the business strikes the financial obligation markets once again, or possibly offers a stake in a few of its equity holdings as it has actually done formerly.

At the minute, I presently have a hold ranking on Intel shares. I do think that we will see enhancement in the total service over the longer term, however this near term assistance was dreadful. While the stock fell on Friday, profits price quotes have actually fallen a lot more, pressing the assessment a fair bit greater. Before actioning in here, I want to see the P/E number be well listed below the Nvidia/ AMD average once again up until Intel gets the development story more on track. In the short-term, shares fell listed below their 50-day moving average at $45.58 on Friday, so I would not be comfy purchasing up until we were closer to the 100-day (near $41 however increasing) to get a few of the technicals pull back from an overbought scenario.

In the end, Intel revealed a strong surface to 2023 however bad assistance for the very first quarter of this year stopped the current rally in its tracks. The worst days for profits and adjusted profits are definitely behind us, however there is still a great deal of work here delegated do. Up until a bit more development is made on the longer term sales photo, in addition to we see the capital scenario swinging back to the favorable for great, the assessment simply does not calm me here.