Christopher Furlong/Getty Images News

My Thesis

You understand, in my nation, we do not have Starbucks ( NASDAQ: SBUX). Each time someone returns from a holiday in the United States or Europe, they discuss that the coffee taste is various. However notice what I composed here– they go to Starbucks and return there on the next trip. Why is that? Well, it’s since Starbucks handled to develop a super-strong brand name power, a status sign. I remember my sibling wished to purchase Starbucks simply for its cup; she does not even like coffee.

Starbucks’ brand name power is equating into numbers and producing a premium business, one that I have an interest in. It has high returns on capital, ones that are growing, strong top-line development, and excellent solvency. It likewise pays a great dividend, although I ‘d choose it to purchase more shares.

However the cherry on top is that it is likewise trading at a sensible cost. Let’s dive in.

Brand Name Moat

I think Starbucks has a moat, even a broad one. I’ll utilize Morningstar Moats to show it.

Intangible Possessions – Though not constantly simple to measure, intangible properties might consist of brand name acknowledgment, patents, and regulative licenses. They might avoid rivals from replicating items or enable a business to charge superior rates.

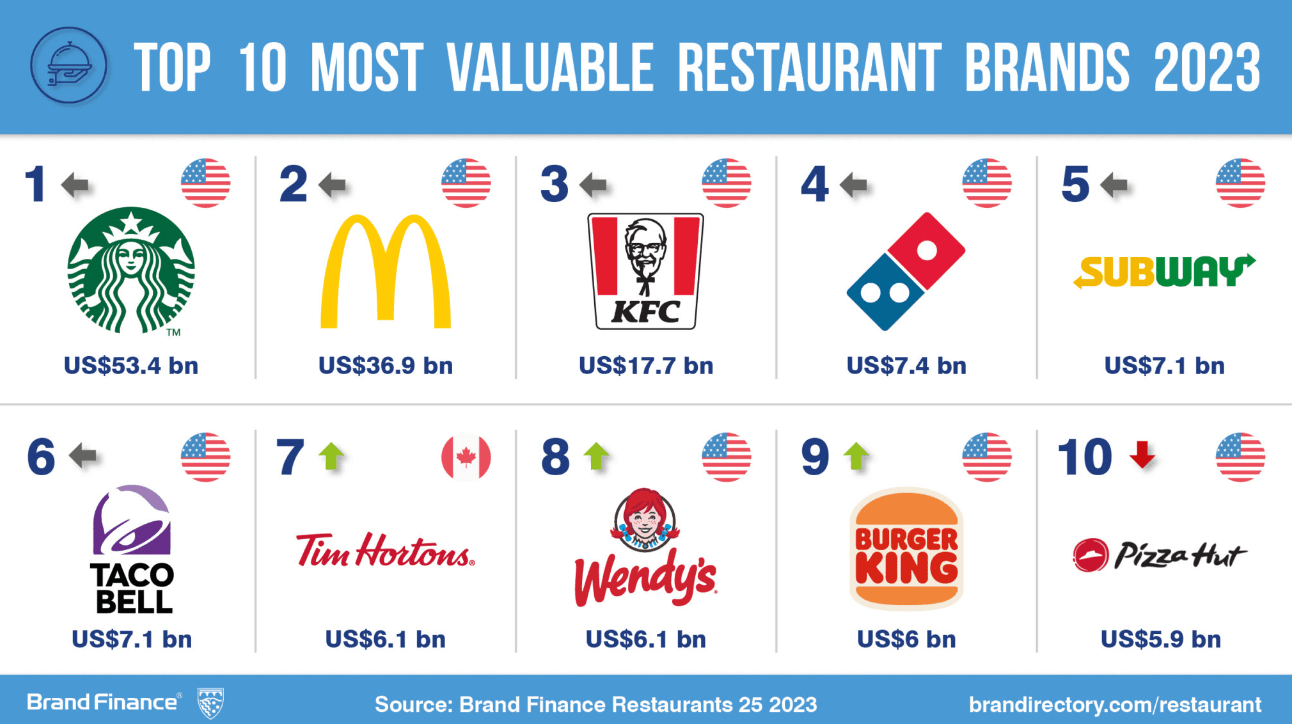

Starbucks has a really strong brand name, probably the greatest in the dining establishment world. In my nation, we enjoy to check out brand names that aren’t readily available here, and the top place individuals go to is Starbucks, primarily for the experience. According to Brand Name Financing, Starbucks is ranked as the number 1 brand name in the market by rather a margin. Structure such brand name power takes some time, specifically to end up being worldwide. This brand name power produces rates power, and rates power is essential when valuing a company. This isn’t simply my viewpoint; even Warren Buffett highlights the value of rates power in company evaluation.

Brand name power ( Brand Name Financing)

We can observe Starbucks’ brand name power in 2023 when individuals had less cash due to increasing rates of interest. In spite of this, Starbucks’ similar sales were strong at 8% year over year, and 9% year over year in The United States and Canada. Here’s a method to evaluate Starbucks’ brand name power: if you stroll the streets of Tel Aviv and reveal the Starbucks logo design, everybody will acknowledge it, whereas if you reveal the Costa Coffee ( KO) logo design, just a few will understand. Another indication of strong brand name power is the at-home coffee market and the ready-to-drink market.

This was driven mostly by At-Home Coffee, while happily holding the top share position in the classification at 16.1%, along with the top position in Ready to Consume, attaining our greatest share in 2 years. Our fall launch, in combination with our The United States and Canada Coffee Collaboration, drove our efficiency, leading to the section carrying out much better than the general classification.

Network Result Moat

Network Result – A network result exists when the worth of a product and services grows as its user base broadens. Each extra client increases the item’s or service’s worth greatly.

Well, Starbucks gain from individuals seeing its logo design on coffee mugs all over. Additionally, as a client, you understand what you’ll get whether it remains in New York City or London– quality coffee. You can rely on the brand name, and with it in every significant city, you go back to purchase there. There are likewise the advantages of the subscription programs, with 33 million members in the United States and an extra 21 million in China.

Our 90-day active Starbucks Benefits members reached a brand-new record this quarter of almost 33 million 90-day active members, and setting records in invest per member and overall member invest. Consumers stay devoted to a preferred 4 menu classics that have actually stood the test of time, consisting of the Pumpkin Spice Latte, which commemorated its 20th anniversary.

Likewise, one might argue that Starbucks has an expense benefit moat due to its massive scale and capability to work out costs. I do not have a method to show it today, so we will not concentrate on this element here.

Leaders

Laxman Narasimhan, the CEO, is brand-new to the task, so we can’t evaluate him so far. Nevertheless, we can take a look at his excellent resume, that includes experience in the retail area and different company locations, speaking with at McKinsey.

What I like about Starbucks is that the board holds super stars, with Satya Nadella, who may not have experience in the dining establishment world, however is a skilled leader I value. Richard Allison, the previous CEO of Domino’s, brings more experience from another strong brand name in the dining establishment area.

CEO rewards are well-aligned with investors, as practically 80% of CEO payment is based upon equity, and more than 90% is at threat. Excellent rewards are really essential in my view, specifically where business is not founder-led or family-owned, and experts do not have substantial ownership, specifically after the famous Howard Schultz left.

Q4, China & & Assistance

Starbucks reported in November and is likewise set to report at the end of the month. Sales grew by 11% year over year in Q4, and when adjusting for currency to evaluate business’s intrinsic efficiency, we see an excellent 14% top-line development. In my view, the more essential numbers are the compensation development rates, boasting an 8% compensation development worldwide, and significantly, a 5% compensation development in the tough Chinese economy. Starbucks prepares to have 9,000 shops in China by 2025, indicating a 15% CAGR in shop growth. Furthermore, there is a possibility that the economy there will recuperate, causing greater compensation development. The management anticipates strong long-lasting development in China. We can observe that the brand name power works well in China.

China now has more than 21 million active commitment members, representing 22% year-over-year development, with numerous members skewing more youthful to develop our next generation of clients …

The momentum versus the background of headwinds in China this previous year offer us optimism in our position and verify our unique competitive benefits for our company …

We continue to see long-lasting development in China with substantial chances in daypart, digital offerings, and shop format and, appropriately, continue to make financial investments for the future of our partners, shops and regional neighborhood.

Likewise, when taking a look at China, the currency-adjusted development looks better and suggests the toughness of business there.

Turning to China. We were pleased with our efficiency in the quarter, providing earnings development of 8% from the previous year, or up 15% when omitting roughly 6% effect of foreign currency translation. This is additional supported by a compensation of 5% directly in line with our expectations. Full-year earnings grew to $3 billion, up 3% from the previous year, or up 11% omitting roughly 8% effect of foreign currency translation with compensation of 2%.

Some might view China as a danger, and I entirely comprehend their issues. As stress with the United States increase, surprises from the Chinese federal government can originate from anywhere.

The assistance was likewise strong, with compensation sales anticipated in the 5-7% variety, continuing the robust development, and around 7% shop count development. Margin growth is really essential in my view, as it can increase Return on Capital figures, a crucial consider long-lasting worth production.

For the approaching outcomes at the end of the month, unless the numbers are substantially off and the management assistance is far from truth, I’ll stay bullish. In Addition, Looking For Alpha information reveals that many experts have actually modified their profits per share projections up.

Numbers

What I’m searching for in a company is strong top-line development with high Return on Capital figures, ideally growing ROC. This mix, in my view, is the greatest worth developer of all. If you handle to capture the stock before numerous growth, you have actually accomplished. Starbucks checks all packages. Experts‘ top-line development price quotes are around 10% substance yearly development rate, comparable to management assistance for 2024. In addition to that, we get margin growth, driven by cost boosts along with functional effectiveness. Management does anticipate margin growth, and with the buybacks, this might cause mid-teens development in EPS. That’s the experts’ agreement also, even up from that.

Margin growth is necessary in my view since it grows the spread in between the business’s Weighted Average Expense of Capital and its ROCE/ROIC figures. A current research study by Michael Mauboussin revealed that business with a high and growing spread in between the WACC and the ROIC tend to carry out well. ROIC depends on how you determine it; management kept in mind at the profits call that Starbucks reached a 25% ROIC. I choose to utilize ROCE since it’s easier and supplies a comparable result. ROCE for Starbucks grew to 28%, an exceptional number.

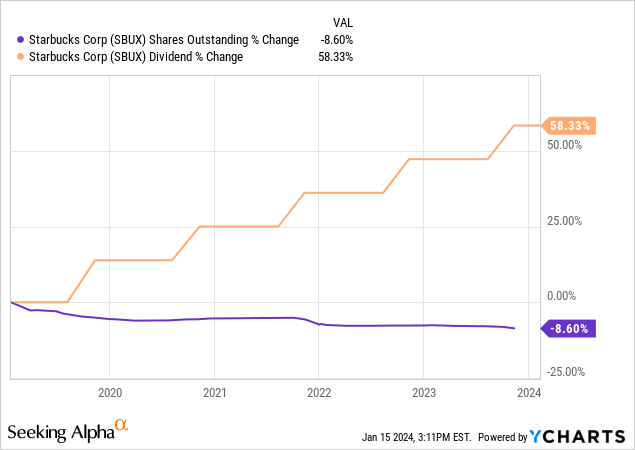

With the additional money, Starbucks returns a lot to investors, with a dividend yield of 2.5%, growing at a 20% CAGR in the last 13 years– a traditional dividend development stock. Management is devoted to a 50% payment ratio. I personally choose buybacks, however money is likewise an ideal choice for me. The development aspect for EPS is the buybacks management undertakes, decreasing the share count by around 1.7% a year.

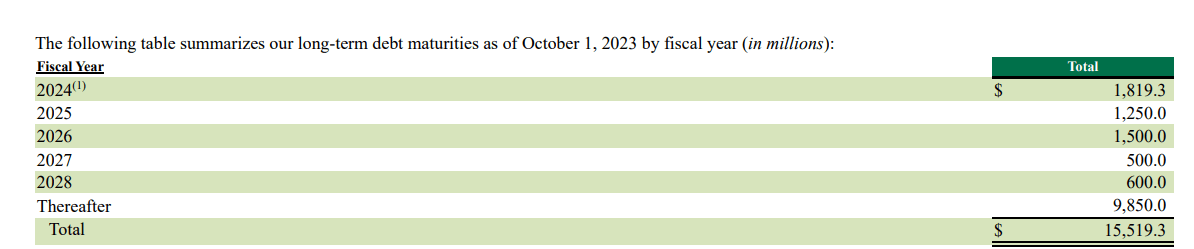

Some might inspect Starbucks’ balance sheet and be worried about the high financial obligation, however I do not view any threat there. Practically $10 billion out of the $15 billion grows after 2028. Starbucks requires to return in between $500 million to $1.8 billion each year, depending upon the year– numbers that are quickly covered by its totally free capital. I do not see this as a danger.

Financial Obligation ( SBUX 10K)

Appraisal

At 22 times NTM profits, it’s inexpensive for a business growing in the mid-teens in addition to a 28% ROCE. In my view, it is really inexpensive. Business with such development capacity are hardly ever discovered at these costs. Another favorable aspect is that Starbucks has space for numerous growths. It is trading listed below its multiples averages, and the capacity for both numerous growth and EPS development in time produces the multi-bagger all of us pursue. A 22 forward PE divided by 16% EPS development offers us a 1.37 PEG ratio, okay for a wide-moat, growing business.

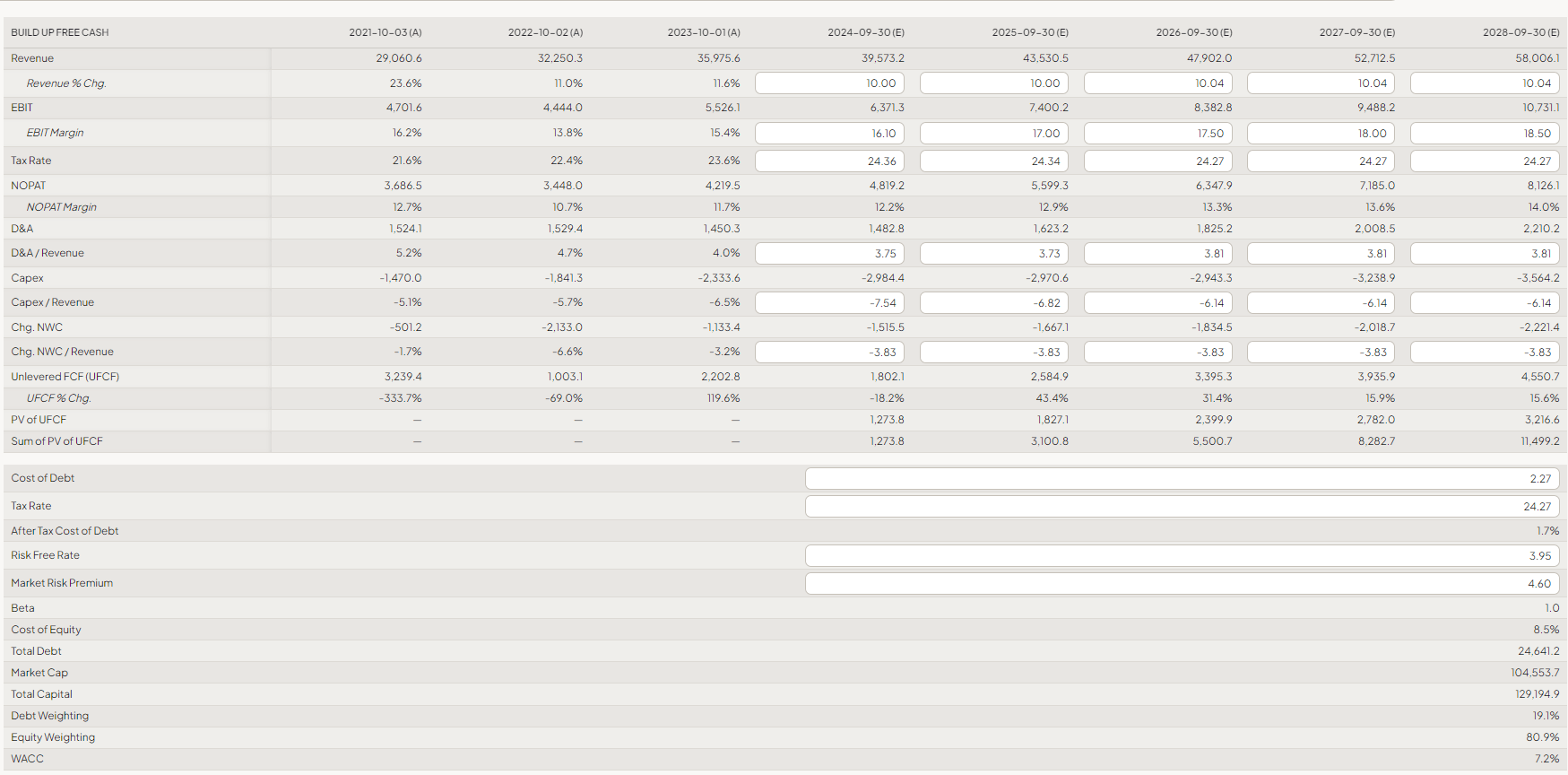

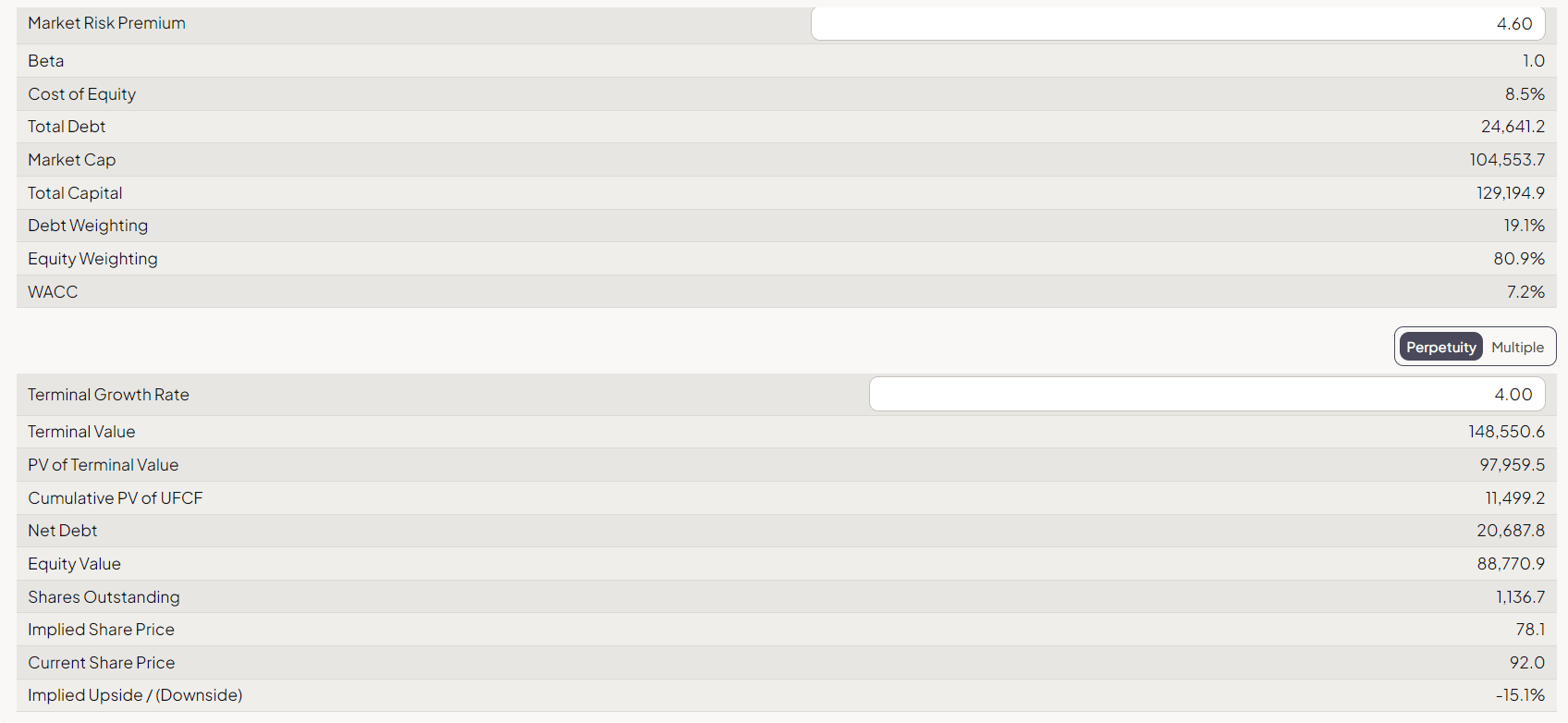

I’ll carry out a DCF analysis, although I’m not a fan since the majority of the time it stops working to catch the worth of such business. Numerous multi-baggers have actually been considered too costly by DCF designs. Utilizing a 7.2% WACC, 4% terminal rate, top-line development of 10%, and a 0.5 basis point margin growth each year, we get a miscalculated stock by 17%. Well, I believe the design is method off, and the business is quite inexpensive.

DCF (FinChat.io)

DCF (FinChat.io)

Dangers & & Conclusions

In spite of the quality of the business, I see a number of dangers:

The very first is the existence of a brand-new CEO and the departure of Howard Schultz. While the brand-new CEO has an excellent resume, a modification in management constantly presents an obstacle.

There are a couple of dangers worrying China, consisting of financial instability and increasing stress with the United States. Nevertheless, the encouraging aspect is that compensation sales are still growing there in spite of the financial downturn.

Another threat is an economic crisis in the United States. Although individuals continue to purchase Starbucks even throughout difficult times, in a serious economic crisis, it’s most likely that individuals may reassess investing $5 on beverages. It is definitely not a recession-proof company, I ‘d state.

Competitors is less demanding for me, as it constantly has actually been, and Starbucks is still at the top.

Thinking about the risk/reward here, I think SBUX is a STRONG BUY for long-lasting investors who will take advantage of a premium, growing company, plus dividends. I eagerly anticipate your remarks.