zhengzaishuru

Nearly 3 years earlier, I suggested purchasing Sabine Royalty Trust ( NYSE: SBR) for an anticipated strong healing from the pandemic. The stock basically tripled in simply 2 years. Nevertheless, back in September and in December, I suggested offering Sabine Royalty Trust due to its high cyclicality and the truth that the energy sector appeared to have actually passed the peak of its cycle. Given that those 2 posts, the stock has actually decreased 17%. This correction might lead some financiers to conclude that the stock has actually ended up being fairly valued. Nevertheless, such a conclusion is extremely dangerous. The stock stays highly valued from a long-lasting point of view while the energy market is going through an unmatched shift from nonrenewable fuel sources to tidy energy sources. For that reason, financiers ought to prevent Sabine Royalty Trust around its existing cost.

Service Summary

Sabine Royalty Trust is an oil and gas trust that was established in 1982, in Dallas, Texas. The business holds royalty and mineral interests in different producing oil and gas residential or commercial properties in Florida, Louisiana, Mississippi, New Mexico, Oklahoma, and Texas.

Much Like all the oil and gas manufacturers, Sabine Royalty Trust has actually considerably taken advantage of the intrusion of Russia in Ukraine, which led the U.S. and European Union to enforce rigorous sanctions on Russia. These sanctions tightened up the worldwide oil and gas markets to the severe in 2015, as Russia was producing around 10% of worldwide oil output and one-third of gas consumed in the European Union prior to the sanctions. Certainly, soon after the execution of sanctions, the rates of oil and gas skyrocketed to 13-year highs. As an outcome, Sabine Royalty Trust more than doubled its overall yearly circulation, from $3.97 in 2021 to an all-time high of $8.65 in 2022. The circulation of the business in 2022 was more than double the circulation of $4.03 in 2013 and 2014, when the cost of oil was hovering around $100.

Nevertheless, the oil and gas markets have actually lastly taken in the effect of the Ukrainian crisis. To start with, the cost of gas has actually plunged this year, mainly due to incredibly low need amidst an unusually warm winter season in the U.S. and Europe. In addition, after the preliminary shock brought on by the sanctions, Russia has actually discovered methods to enhance its production, as it has actually increased its sales of petroleum to China, India, and a couple of other nations. In truth, Russia was just recently reported to be on the cusp of exceeding Saudi Arabia as the greatest oil provider to China. As an outcome, the worldwide oil market has actually progressed provided and for this reason the cost of oil has actually plunged almost 50% off its peak, which was published early in 2015, soon after the start of the Ukrainian crisis.

OPEC has actually tired its methods to support the cost of oil. To be sure, the cartel has actually carried out numerous production cuts in order to supply a strong flooring to the cost of oil. In addition, Saudi Arabia just recently threatened those who short the cost of oil that they will sustain serious losses if they continue shorting the cost of oil. Nevertheless, I think this risk plainly indicates that Saudi Arabia hesitates of an additional decrease in the cost of oil. If Saudi Arabia were positive in the strong principles of the oil market, it would not require to threaten traders, in my viewpoint.

It is likewise crucial to keep in mind that the whole world has actually considerably accelerated its shift from nonrenewable fuel sources to renewable resource sources. According to a current report of the International Energy Administration (IEA), 2023 will be the very first year in which the worldwide financial investment in tidy energy sources will go beyond the worldwide financial investment in nonrenewable fuel sources by about $0.7 trillion. More specifically, about $1.7 trillion is anticipated to be purchased tidy energy sources, whereas just $1.0 trillion is anticipated to be purchased nonrenewable fuel sources. 5 years earlier, the ratio of financial investment in tidy innovations to financial investment in nonrenewable fuel sources was around 1:1, today this ratio has actually skyrocketed to 1.7. This nonreligious pattern unquestionably does not bode well for the rates of oil and gas in the upcoming years.

Circulation

Due to the natural decrease of oil and gas fields, the production of Sabine Royalty Trust tends to reduce in the long run. To be reasonable, when the trust was established in 1982, it was anticipated to have a life time of about a years. As the trust is still producing significant quantities of oil and gas, 4 years after its initiation, it appears that the trust has actually gone beyond the preliminary expectations by a remarkable margin. However, a decline in the production of Sabine Royalty Trust is inescapable in the long run, as the trust can not broaden into brand-new locations, unlike the widely known oil majors. For that reason, all else being equivalent, the circulation of Sabine Royalty Trust is most likely to reduce in the long run. The outlook is even worse if the nonreligious shift from nonrenewable fuel sources to tidy energy sources is taken into consideration.

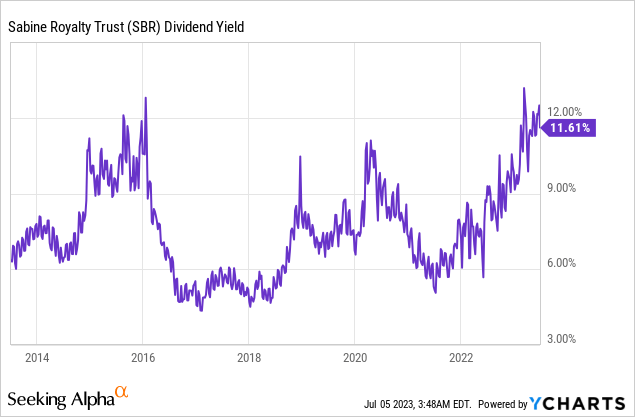

Due to the danger that arises from its long-lasting decreasing output, Sabine Royalty Trust has actually constantly used an above-average circulation yield.

Throughout 2013-2019, Sabine Royalty Trust used a typical yearly circulation of $ 3.13 This is a reputable figure for the long-lasting capacity of the trust, as this 7-year duration was regular in recommendation to the rates of oil and gas. The current years have actually been drastically unstable, as the rates of oil and gas collapsed in 2020 due to the pandemic and skyrocketed in 2021 and 2022 thanks to the healing from the pandemic and the Ukrainian crisis. Whenever the cost of oil go back to regular levels, one can fairly anticipate the yearly circulation of Sabine Royalty Trust to go back to about $3.13. At the existing stock cost, this circulation represents a 4.8% yield. This yield is much lower than the historic typical yield of the stock, and for this reason, the stock cost of Sabine Royalty Trust is most likely to reduce substantially off its existing level to lead to a regular (near to the historic average) yield.

Based upon its regular monthly circulations in the last 12 months, Sabine Royalty Trust has actually used a circulation yield of 12.5%, based upon its existing stock cost. Nevertheless, the trust is not most likely to use such high circulations anytime quickly due to the sharp correction of product rates. In truth, the most recent regular monthly circulation of the trust represents an annualized yield of just 6.0%. While this yield might appear high to many financiers, it is not appropriate to compensate financiers for the danger associated to the long-lasting decrease of the production of the trust.

Last Ideas

Sabine Royalty Trust has actually shown excellent company efficiency throughout its life time, as it has actually gone beyond the preliminary expectations for its period by a large margin. Nevertheless, the circulations of the trust are highly connected to the cycles of the rates of oil and gas. The oil and gas market appears to have actually passed the peak of its cycle for great, and its outlook is unfavorable due to the sped up shift of the whole world from nonrenewable fuel sources to renewable resource sources. While nonrenewable fuel sources will stay the main energy source for many years, the shift to tidy innovations is most likely to affect the rates of oil and gas in the upcoming years. For that reason, while nobody can leave out a short-term bounce of Sabine Royalty Trust (it is difficult to forecast the course of stock rates in the brief run), the stock stays dangerous from a long-lasting perspective.