Uriel Sinai/Getty Images News

Rocked By Pessimism

Searching pharmaceutical stock reports to upgrade our post about Teva Pharmaceutical Industries Ltd. ( NYSE: TEVA), we are struck by the extremely unfavorable belief. Articles produce a variety of barbed remarks. In spite of headwinds, we see bullish capacity with dangers that make TEVA stock worth a Buy chance score at under $8 per share. Otherwise, we believe the stock is best defined by a Hold score.

Experts on TEVA ( seekingalpha.com/symbol/TEVA)

Disadvantages

Teva management has little to crow ready to investors. They deal with a huge battle to alter the dominating bearish viewpoints. For example, commenting on a report about a rejection letter from the USFDA for AVT02 BLA to TEVA in April 2023, one reader composed, “Who in the world will purchase Teva? It’s a cash ruining maker. Not to discuss it’s part in the opioid crisis in the U.S.A. (for those who think about ethical[ity] in their financial investments).”

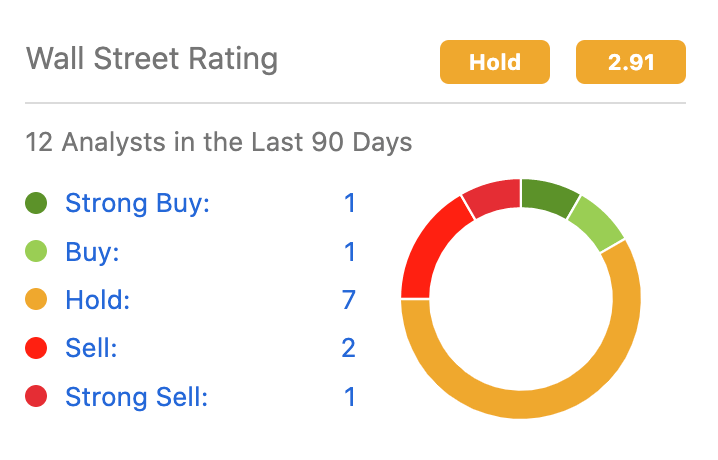

2nd, experts are downhearted. 11 of 12 experts surveyed by Looking for Alpha rate TEVA stock at Hold, Offer, and Strong Offer. 11 of 17 experts covering the stock are reported in other places to have actually ranked TEVA at Hold through February and March ’23. One had it lower in January at Underperforming. In April, 17, up from 11, appoint the stock a Hold score. 5 others offer it an Underperform.

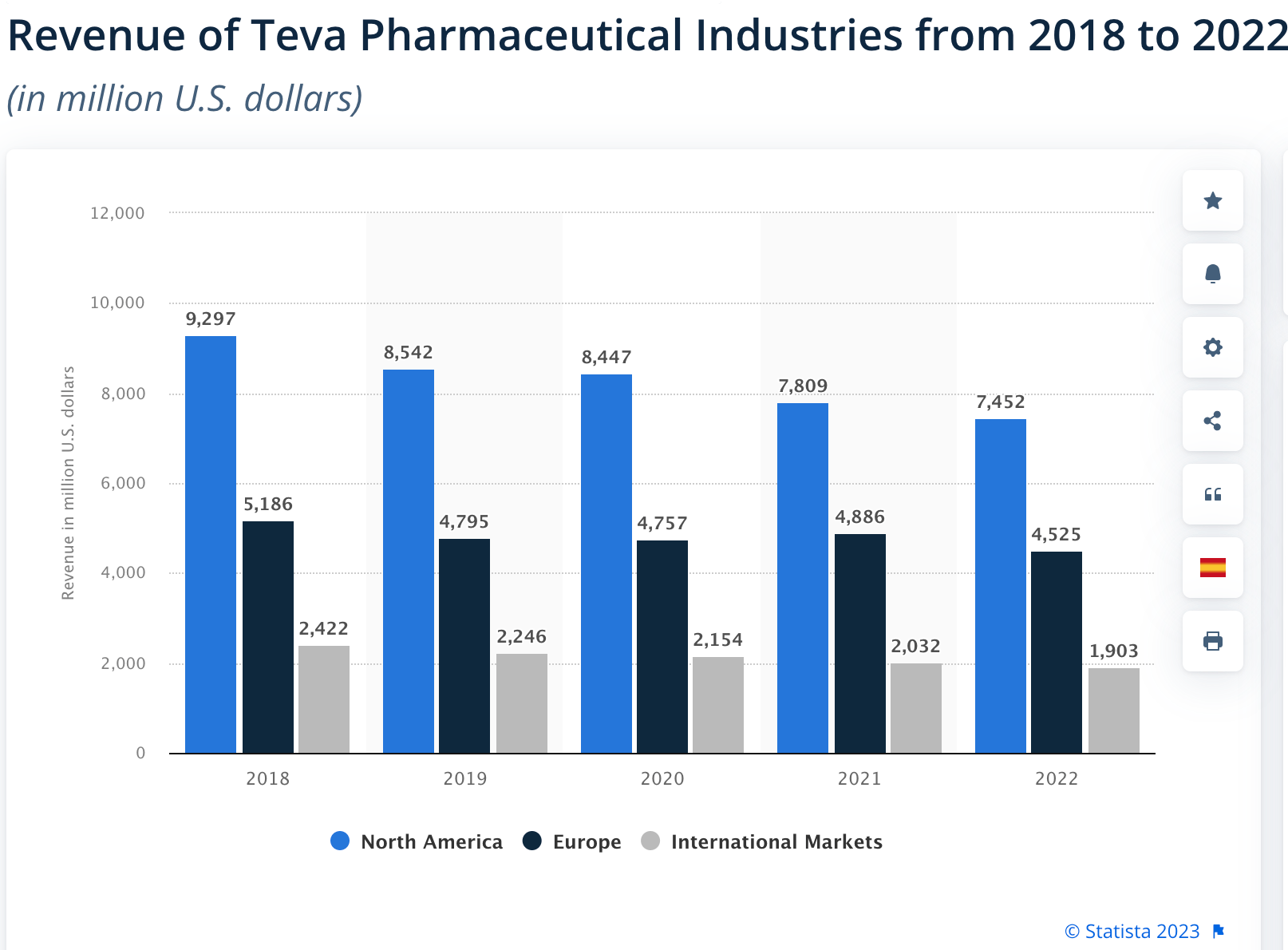

The 3rd disadvantage is the 5-years long drop in income. The pattern continues in spite of the international market for generics growing at a CAGR of 5.6%. Teva Pharmaceutical Industries slipped from the primary generic drug maker by income in 2021. It is now second amongst the leading 5 generic-producing business. Pharmaboardroom.com explains Teva’s condition in this manner:

Rx Sales: USD 19.468 billion– Can be found in at second is Israeli giant, Teva. After rough times that included overcoming significant financial obligation and paying a United States opioid settlement, the business continues to see slipping profits. Recently designated CEO Richard Francis still has his work cut out for him as international sales have actually decreased and Teva created USD 14.93 billion in 2022, a 6 percent decrease from USD 15.88 billion in 2021. The business is banking on the increasing sales of its Austedo, authorized for Tardive dyskinesia and chorea from Huntington’s illness, which grew by 22 percent in 2022, and its migraine avoidance drug Ajovy.

Q4 ’22 income was $3.9 B or -5.3% from Q4 ’21. The GAAP bottom line in FY ’22 was $2.35 B compared to a GAAP net revenue of +$ 400M in 2021. In spite of the headway made in paying for financial obligation, financial obligation stays significant. It can possibly end up being more challenging in a duration of increasing rates of interest, tightening up financing practices, and virtually no boost in income. If an expected economic downturn strikes hard in the United States and in Israel, customers will have less money to invest in co-pays. Less in the United States will have insurance coverage to purchase brand-name or generic drugs.

Teva Markets ( statista.com/statistics/272550/revenues-of-teva-pharmaceutical-industries-by-region/)

A 4th headwind for Teva is lower than chosen credit rankings which produce greater loaning expenses. Fitch Rankings has Teva Pharmaceutical Industries’ long-lasting default and its senior unsecured credit center rankings at BB- for almost all the concerns raised above by Pharmaboardroom.com. Moody’s designates Ba2 score to Teva’s brand-new senior notes.

A 5th disadvantage for investors is the money and item payments the business is going to start making by the end of 2023 on its $4.25 B opioid lawsuits settlement (~$ 400M annually over 13 years). That Teva Pharmaceutical does not pay a dividend might alleviate the interest amongst retail worth financiers.

In whenever of international financial downturn and duration of increasing joblessness, it is our experience the strong business get more powerful and the weak get weaker. Hedge funds offered about 6M shares last quarter. The variety of funds holding shares is steady over the last couple of years. Their number increased from 29 funds in Q3 ’22 to 31 entering into 2023. The next incomes report will be revealed on May 10, 2023.

Stability and Possible

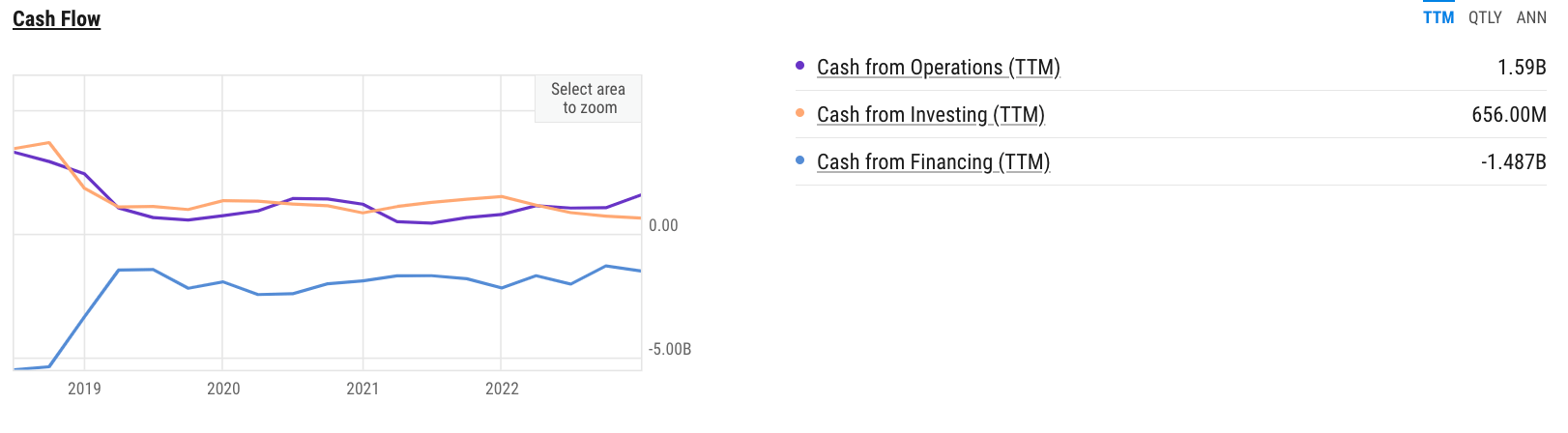

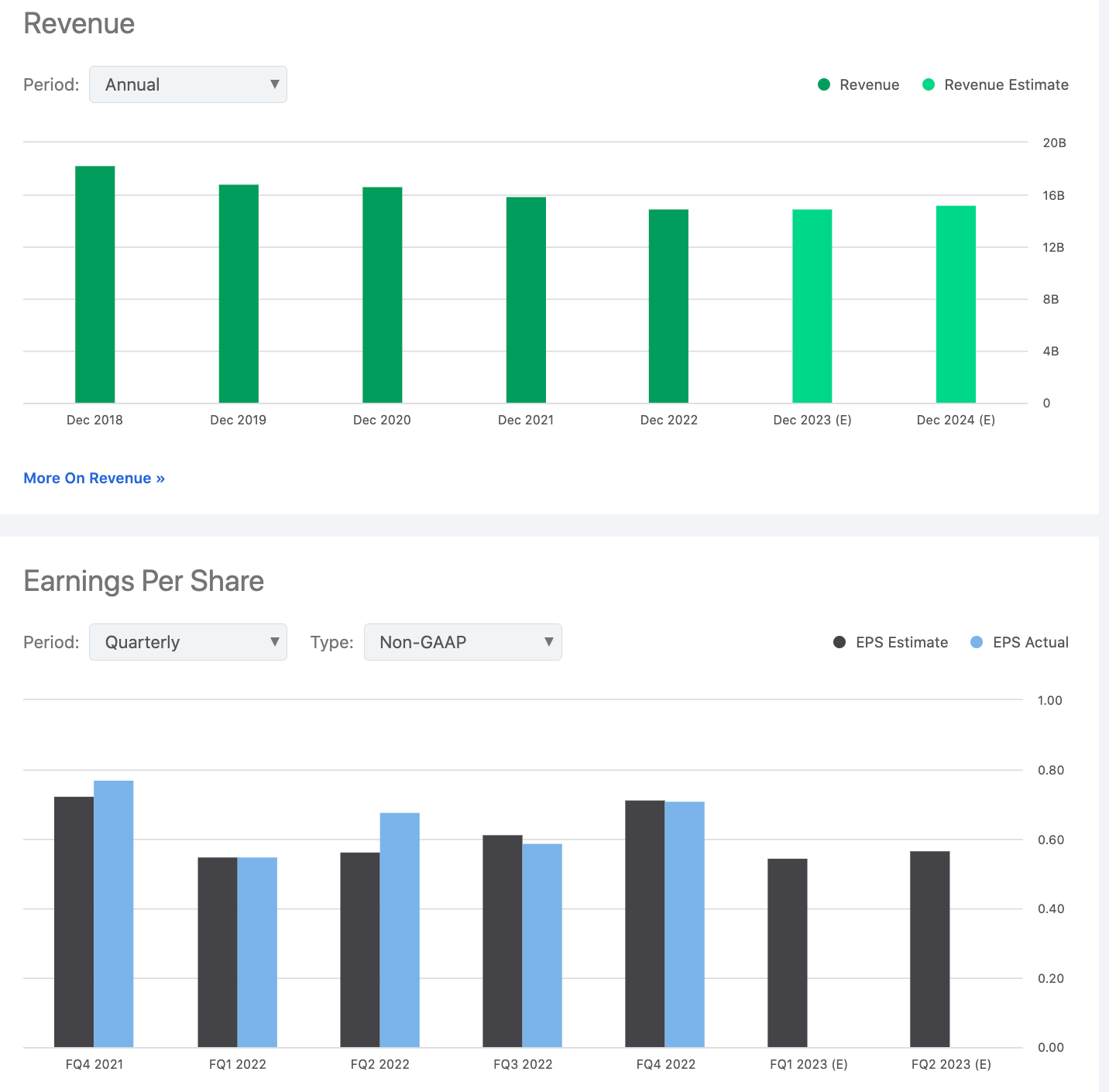

In August 2015 the stock topped $70 per share. It offers today nearer to its 52-week low of $6.78 than to its high at $11.45 months back. It has upside possible from the ~$ 8.35 present asking price per share if what management informs us they anticipate for FY ’23 is sensible; that is, income is anticipated to be $14.8 B to $15.4 B, the adjusted EBITDA is anticipated at $4.5 B to $4.9 B, and the non-GAAP diluted EPS is anticipated to be $2.25 to $2.55. FY ’21 capital was $798M. It virtually doubled in 2022 after the business offered receivables. Totally free capital is anticipated to be $1.7 B to $2.1 B.

Teva Capital ( ycharts.com/companies/TEVA)

Improving income and incomes price quotes is crucial if investors are to benefit. We believe the brand-new CEO is smart in offering conservative price quotes and assistance for 2023.

We aim to the SA Element Grades for Teva. Just for development does Teva get a D-; that is below A- 3 months back and 6 months previously. All other Element Grades are strong and support our reasonably bullish position: B- for momentum, A for success, and B for evaluation. SA’s Quant Score of Hold tilts towards a Buy evaluation.

Brief interest is simply 1.48%. Our company believe the disadvantages are factored into the share cost. The PE is 3.46. Other elements making up the evaluation, other than for PEG non-GAAP that gets a C-, are high marks. If management can decrease dangers and raise more income and incomes, we anticipate a typical cost target over the next 9 months of $9 to $9.45. We merely take the P/E and increase it by an approximated EPS for 2023 and include into factor to consider the SA strong Element Grades.

Profits & & Revenues Projections ( seekingalpha.com/symbol/TEVA)

Positivity is Returning

TEVA stock is -78% over ten years, -52% over the last 5 years, -11% to 12.7% over the last 12 months and YTD, respectively. Investors suffered tremendously from bad management choices and disability expenses, $1.3 B in Q4 ’22 alone. Pessimism is plentiful however there are favorable indications meaning revenue capacity.

Concerning credit rankings, Fitch Rankings has Teva Pharmaceutical Industries’ long-lasting default and its senior unsecured credit center rankings at BB-. Fitch’s outlook defines the business as steady. Moody’s designates Ba2 score to Teva’s brand-new senior notes as steady however with speculative components and credit danger.

Our 2nd factor to up our evaluation of Teva involves its significant possessions. Size is an aspect; the marketplace cap is over $9B. Teva offers a portfolio of around 3,600 items utilized everyday by almost 200M individuals in 60 nations every day. The business sports a great track record for quality assurance. Teva claims to offer generics to three-fourths of the leading 50 pharma business. The trademark of its operations is R&D and developments. It has a strong market share, especially in the United States pressure is growing for broader usage of generics.

An extrinsic favorable note for Teva Pharmaceutical Industries might be struck by the United States federal government. The administration is under significant pressure to lower Medicare and Medicaid drug expenses. Republicans and Democrats are advocates of generic drugs pressing the administration to cut costs and lower out-of-pocket drug expenses by broadening using generics.

The 3rd favorable aspect our company believe Teva is turning things around is management’s projection that sales will tick up 1.1% in 2023 after 5 years of falling sales. For circumstances, Financier’s Organization Daily reports the Teva drug Austedo which deals with tardive dyskinesia, an uncontrolled motion condition, created $963M in sales in 2022, up 20% Y/Y. The CEO informed experts sales of the drug can reach $1.2 B in 2023.

2 other drugs, Copaxone and Anjovy can produce $500M and $400M, respectively. In 2015, Ajovy sales popped 24% to $218 million. Management likewise anticipates to launch this year a biosimilar for arthritis treatment, Humira, pending U.S. regulative approval, to increase income.

Third, some experts are cogitating about the future of Teva Pharmaceutical Industries. KÃ¥re Schultz, its previous CEO because 2017, took the reins at a deep-well low point. His 5-year stint in charge will make an exceptional company case research study in crisis management. He introduced an efficient cost-cutting project, the architecture of which exists in 2023 and remains in big part the factor for the business’s significant and acknowledged financial obligation decrease.

Experts at Israel’s and another at America’s biggest banks are favorable about Teva Pharmaceutical Industries. They recommend it deserves a Buy score. Informing Israel’s Globes news last February, the cost target of $13 per share or ~ 30% greater can be attained. Teva’s “assistance for 2023 remains in line with expectations on sales, EBITDA, and complimentary capital.”

Our company believe TEVA is an underestimated stock. It is a prospective chance for retail worth financiers with a great step of danger tolerance, though our company believe the shares are at low danger of decreasing much even more. Modest development will send this stock greater.