Our inebriated sailors in Congress much better head to the detox.

By Wolf Richter for WOLF STREET

The superbly swelling United States federal government financial obligation is quickly approaching $34 trillion (now at $33.84 trillion), up from $33 trillion in mid-September, and up from $32 trillion in mid-June, in the middle of a tsunami of issuance of Treasury securities to money the sensational federal government deficits.

However inflation has actually broken out on an enormous scale in early 2021, and the Fed has actually treked its policy rates to 5.5% on top end, and it has unloaded $1.1 trillion from its balance sheet under its QT program, which is rising long-lasting yields. Therefore the rates of interest that the Treasury Department needs to pay to be able to offer these mountains of Treasury securities weekly has actually increased, with T-bills costing yields of around 5.5% and longer-term securities selling at yields in the 4.3% to 4.7% variety, after discussing 5% a month back.

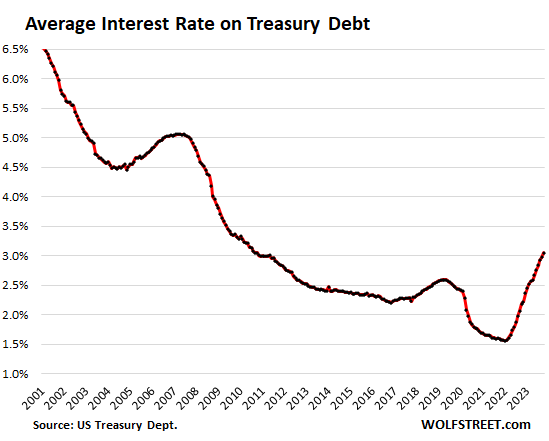

So the typical rate of interest that the federal government is paying on all its interest-bearing financial obligation– much of it provided years ago with much lower discount coupon rates of interest than now– has actually been increasing from the historical low of 1.57% in February 2022 to 3.05% in October, according to information from the Treasury Dept.

This typical rate of interest will continue to increase as brand-new securities with greater rates of interest change growing lower-interest rate securities that were provided frequently years back, and as all the freshly included financial obligation is overdone at the existing greater rates of interest.

The securities provided just recently will cost the federal government whatever discount coupon interest they included till they develop. The $40 billion of 10-year Treasury notes that were cost the November 8 auction with a yield of 4.52% will cost the federal government 4.5% in discount coupon interest payments for the next ten years, no matter what occurs to rates of interest.

The interest concern gets much heavier. How heavy?

Interest payments reached $245 billion (not seasonally changed) in Q3, having actually doubled given that 2018. However the economy has actually grown a lot, work has actually grown, a record variety of individuals are working, and they’re making record quantities of cash, and they have actually gotten the greatest pay boosts in 40 years, and inflation has actually removed, and business revenues have actually swollen, and there were substantial capital gains in 2020 and 2021, all of which set off huge quantities of tax invoices.

In 2022, markets handed financiers a lousy offer, and capital-gains tax invoices in Q1 and Q2 this year for the tax year 2022 plunged, even as other earnings taxes continued to rise. And these tax incomes need to be utilized to spend for the interest on the financial obligation.

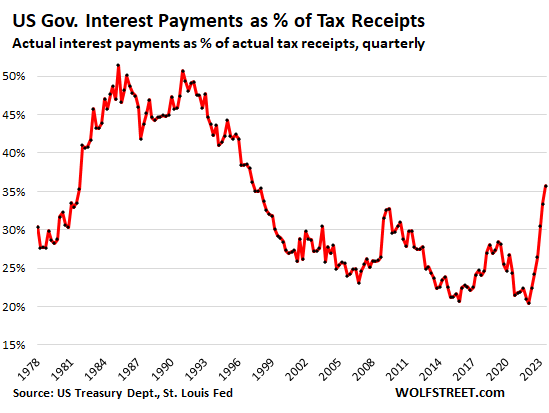

Interest payments as % of tax incomes is the main procedure of the concern of the nationwide financial obligation on federal government financial resources. This procedure of tax incomes– overall tax incomes minus contributions to Social Security, other social insurance coverage, and some other elements– was launched today by the Bureau of Economic Analysis as part of its GDP modification. This part of the tax incomes is what’s readily available to spend for routine federal government expenses, consisting of interest cost.

The ratio of interest cost as percent of tax incomes increased to 35.7% in Q3, up from 24.3% a year back, and back where it had actually remained in Q2 1997. However:

- The spike was from the 20.4% in Q1 2022, the most affordable given that 1969.

- In the 15 years in between 1982 and 1997, the ratio was greater.

- In the ten years in between 1983 and 1993, the ratio varied from 45% to 52%.

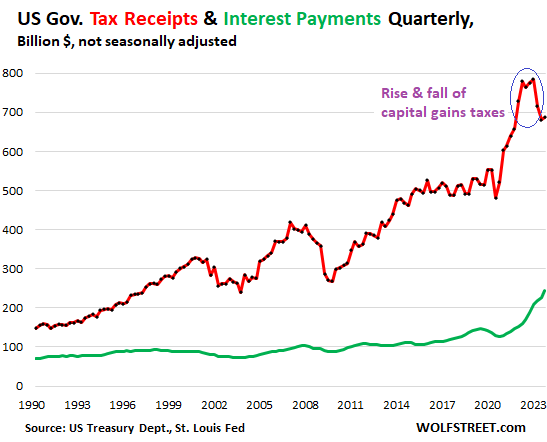

Tax incomes ( minus contributions to Social Security, other social insurance coverage, and some other elements) increased to $687 billion in Q3, after having actually dropped in Q1 and Q2 on plunging capital-gains tax incomes following the bad year 2022 for stocks, bonds, cryptos, and other financial investments.

The plunge of the capital acquires taxes was off the top of the Fed-fueled asset-price spike in 2020 and 2021 (red line in the chart listed below).

Interest payments leapt to $245 billion in Q3, on the ballooning financial obligation moneyed with greater typical rates of interest (green).

This chart takes into point of view the interest payments and the tax incomes (minus contributions to Social Security, other social insurance coverage, and so on) that are readily available to make those interest payments.

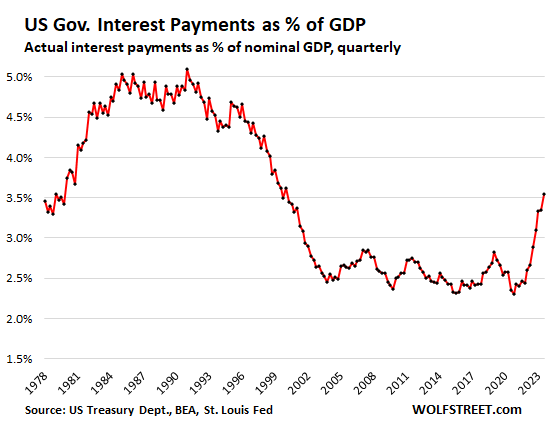

Interest payments as percent of GDP increased to 3.5% in Q3, based upon today’s modified nominal GDP for Q3.

The ratio is figured on an apples-to-apples basis: quarterly interest cost not changed for inflation, not seasonally changed, not yearly rate; divided by quarterly small GDP ($ 6.93 trillion in existing dollars) not changed for inflation, not seasonally changed, not yearly rate.

The ratio of 3.5% was the greatest given that 2000, however well listed below the variety in between 1979 and 2002, when it had actually peaked at over 5%, and remained above 4.5% for almost 15 years.

So, this is a gruesome spike, however off extremely low levels, and not yet in the headache area of the 1980s. However at the existing rate of development, the spike may reach those headache levels in a number of years.

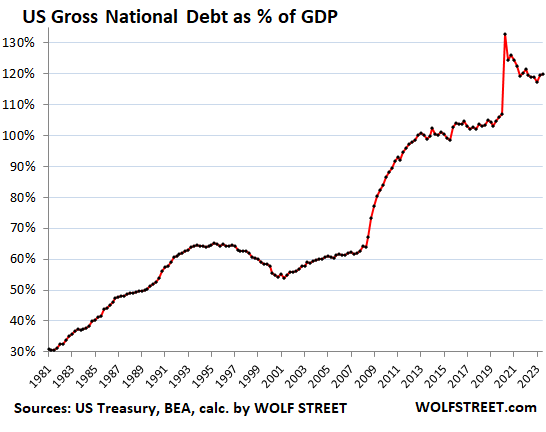

The United States nationwide debt-to-GDP ratio increased to 120% in Q3. So this procedure is not affected by interest payments or rates of interest. This is the overall gross nationwide financial obligation at the end of Q3 (not changed for inflation) divided by small GDP (seasonally changed yearly rate, not changed for inflation).

The spike in Q2 2020 to 133% had actually happened primarily since GDP had actually collapsed, and to a lower degree since the financial obligation had actually leapt.

If small GDP grows faster than the financial obligation, the ratio decreases, and for that reason the concern of the financial obligation decreases, as it has actually done after Q2 2020.

However in Q3, small GDP grew by 2.1% from the previous quarter (not annualized, not changed for inflation), while the financial obligation grew by 3.5% over the exact same duration (likewise not annualized, not changed for inflation). Therefore the concern of the financial obligation grew. A comparable thing took place in Q2.

High interest concern may send out Congress into Detox, however not yet Back in the 1980s through early 1990s, the concern of interest cost consuming half of the federal tax incomes (minus social insurance coverage), while bond vigilantes were trotting around nervously, set off a great deal of handwringing in Congress and ultimately required Congress to start coming to grips with truth. Ultimately, they lowered the deficits.

High interest concern may be the only discipline left that can press our inebriated sailors in Congress into detox to sober up. However it’s not taking place yet. Our inebriated sailors in Congress– “our” since we put them there, and we provide the alcohol– are still partying, and they’re brushing off the grandstanding about the financial obligation in some corners.

The Fed’s function in this mess With its careless interest-rate repression from 2008 through 2021, through near-0% policy rates and trillions of dollars in QE, the Fed has actually motivated Congress to go on an impressive deficit-spending binge since the financial obligation does not actually matter when the expense of loaning is near absolutely no. Now it all of a sudden matters, and it will matter a lot more moving forward.

Enjoy reading WOLF STREET and wish to support it? You can contribute. I value it profoundly. Click the beer and iced-tea mug to learn how:

Would you like to be alerted through e-mail when WOLF STREET releases a brand-new post? Register here

![]()