FatCamera/iStock through Getty Images

Ingenious Industrial Characteristic ( NYSE: IIPR) is among the more fascinating REITs on the marketplace today.

With a significant dividend of almost 8% and an organization design that obtains its earnings from an ‘off the beaten course’ market, some might be questioning whether this business has what it requires to make an area in their portfolio.

Today, we’ll take a more detailed take a look at IIPR, and identify whether the business is well placed from a monetary perspective.

Can the REIT maintain its remarkable circulations? Exists space for capital gratitude? Let’s dive in and figure it out.

Financials

The very first think here is the business’s financials, which remain in respectable shape, all things thought about.

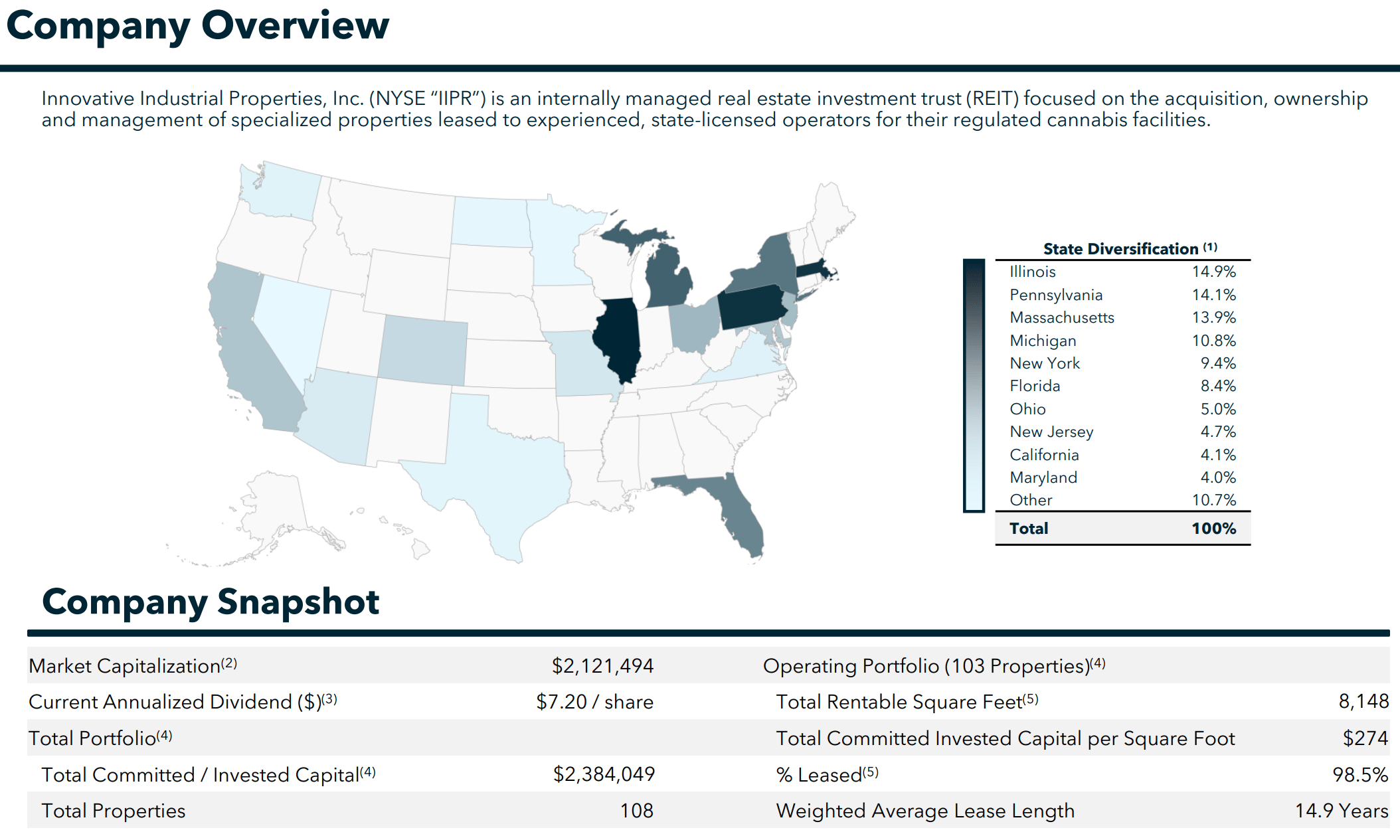

In case you’re brand-new to IIPR, the business is a REIT, whose property holdings are primarily consisted of specialized residential or commercial properties tailored towards marijuana production and processing:

Financier Discussion

This consists of 103 centers throughout 18 states and 8.1 million in overall square feet.

On the plus side, the company has a really low LT Financial obligation/ Capital ratio of just 13%. This low level of insolvency suggests that most of IIPR’s incomes can drop best to FFO, and therefore, to financiers’ pockets.

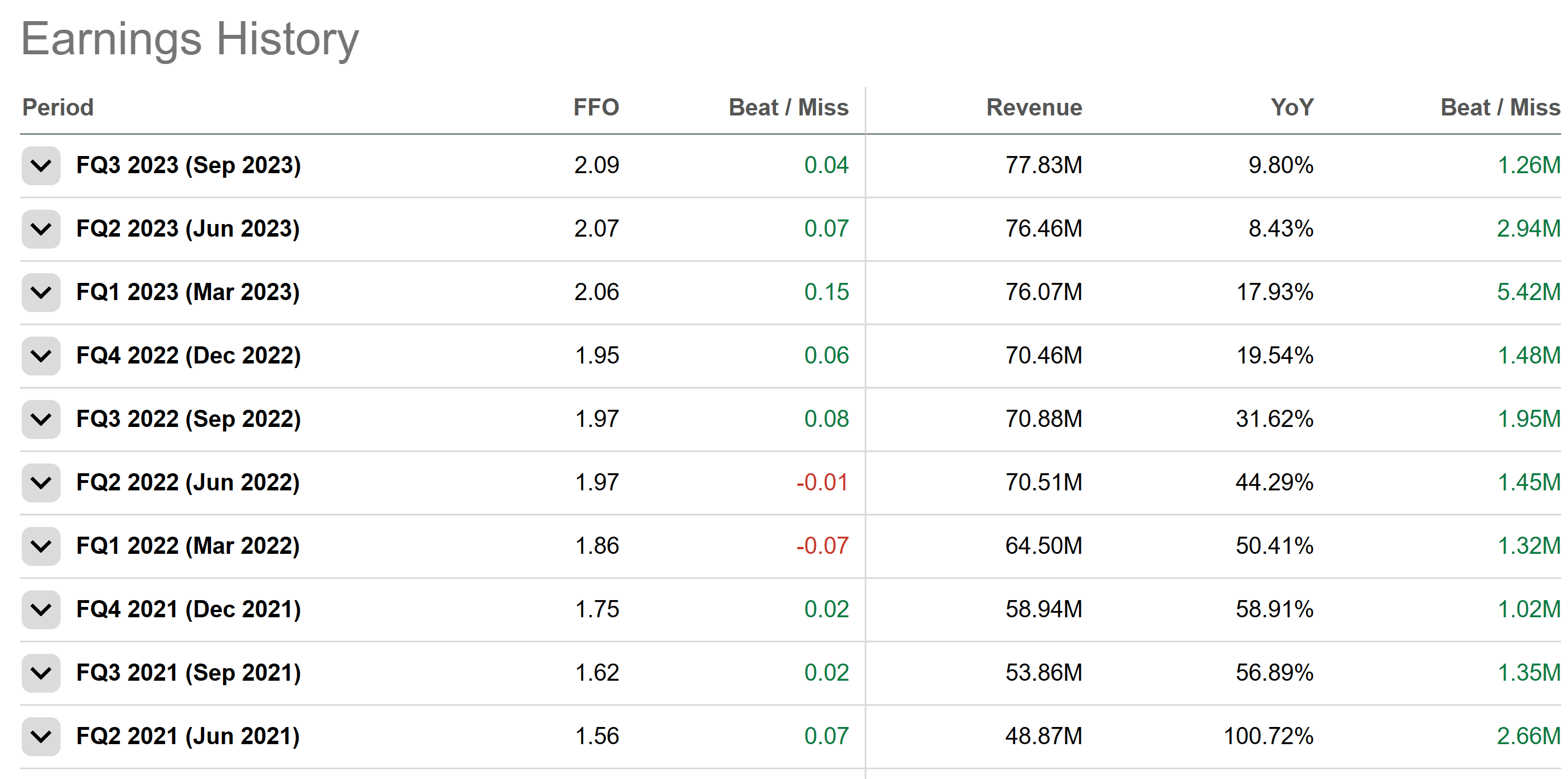

Earnings-wise, the business has actually done effectively over the last a number of years, beating leading line sales regularly and just missing on EPS two times:

Looking For Alpha

On the other side, income development is slowing substantially, from 58% in Q4 of 2021 to upper single digits over Q2 and Q3 of 2023.

This slowing down income is mostly due to the absence of brand-new capital being invested into the area, together with occupant difficulties which have actually been injuring monetary efficiency.

Here’s a good summary of that from The Dividend Collectuh in their current post:

Ingenious Industrial has actually been handling occupant difficulties for a while now. Previously this year, the REIT had occupants Parallel & & Green Peak Industries default on residential or commercial properties. They likewise had affiliates of Medical Financier holdings default on among their California residential or commercial properties. Throughout the last quarter management mentioned they had actually reclaimed residential or commercial properties from Parallel, Green Peak, and King’s Garden.

In concerns to Green Peak, IIPR restored ownership of 2 little retail residential or commercial properties rented to the business and anticipates to restore ownership of another at the end of this month. Management did state they offered Green Peak’s properties to a purchaser this previous October. These distressed occupants triggered tenancy rates to drop over the previous couple of quarters.

In amount, it’s been a rather unstable time for IIPR’s occupants, however things are anticipated to enhance moving forward, now that IIPR is back in ownership of its residential or commercial properties and ought to have the ability to re-rent those centers.

This was highlighted on the current revenues call, where Chairman Alan Gold stated the following:

We have among the greatest and most skilled groups of property experts in the marijuana market, a premium portfolio and perhaps a conservative and versatile balance sheet, with a 12% financial obligation to overall gross properties, no variable rate financial obligation, no significant financial obligation maturities till Might 2026.

…

To summarize the quarter, we produced overall incomes of $78 million in Q3 and changed funds from operations of $65 million. Lease collection for IIP’s operating portfolio was 97% for the quarter. The monetary efficiency continued to drive dividend go back to our financiers with $7.20 of dividends stated per share in the previous 12 months, a boost of 6% over the previous 12-month duration.

From lots of angles, the ship seems righting.

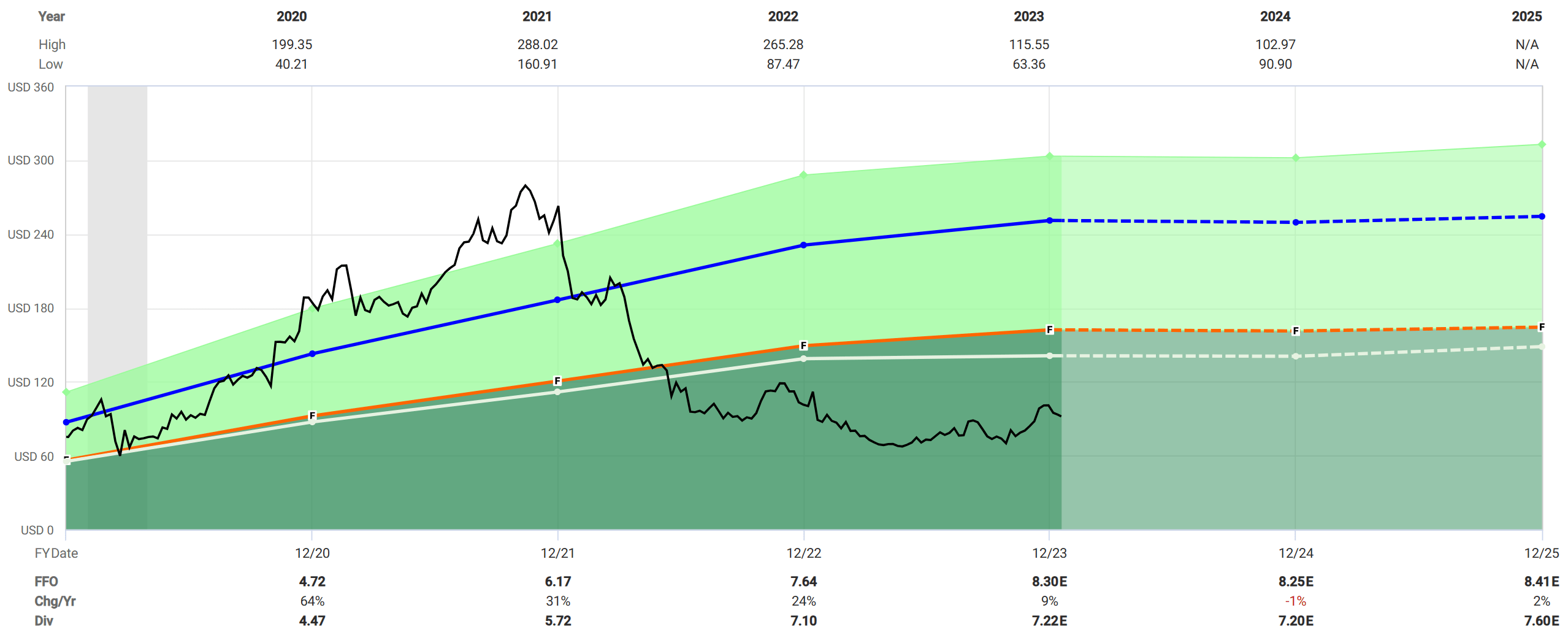

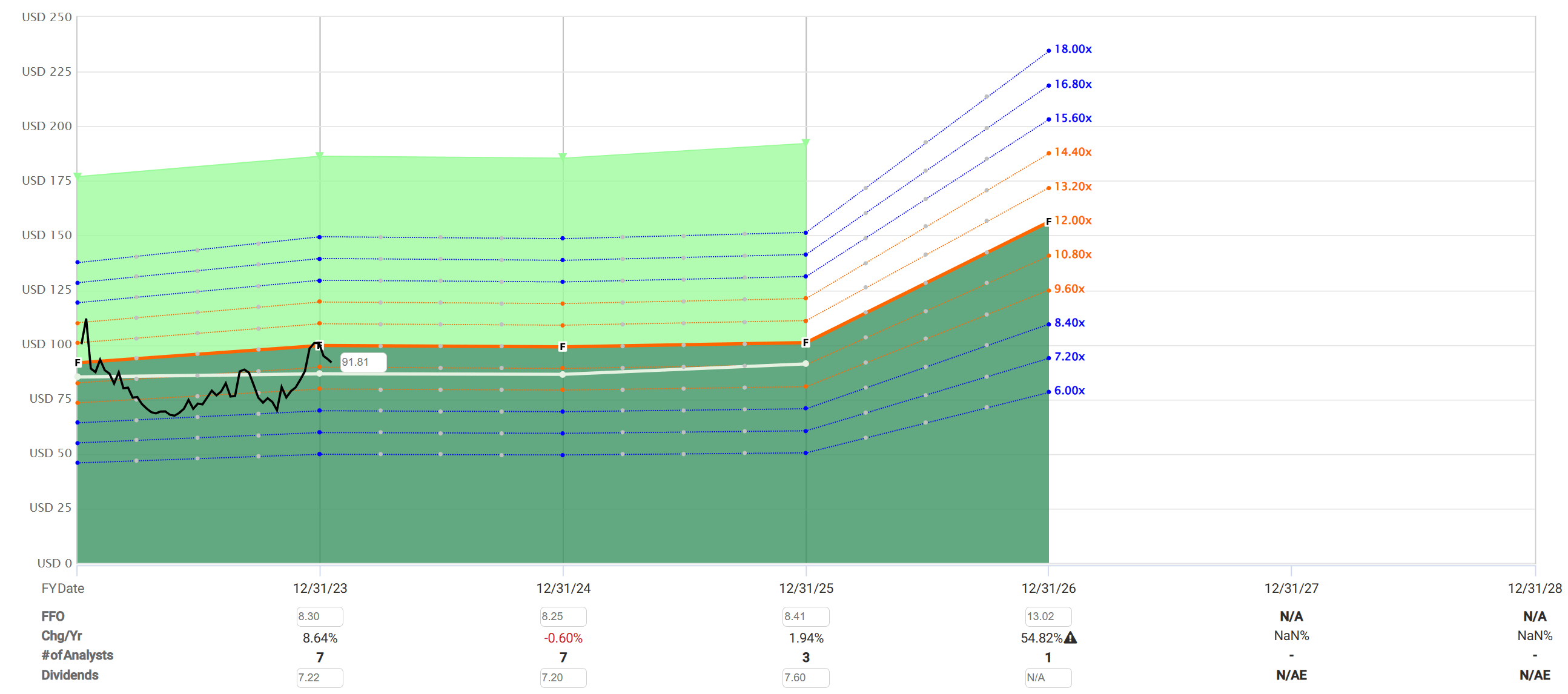

You can see this if you start to look more carefully at IIPR’s anticipated development rates, which are a hair unfavorable for 2024, however are anticipated to reverse to the favorable side in FY 2025:

Quickly Charts

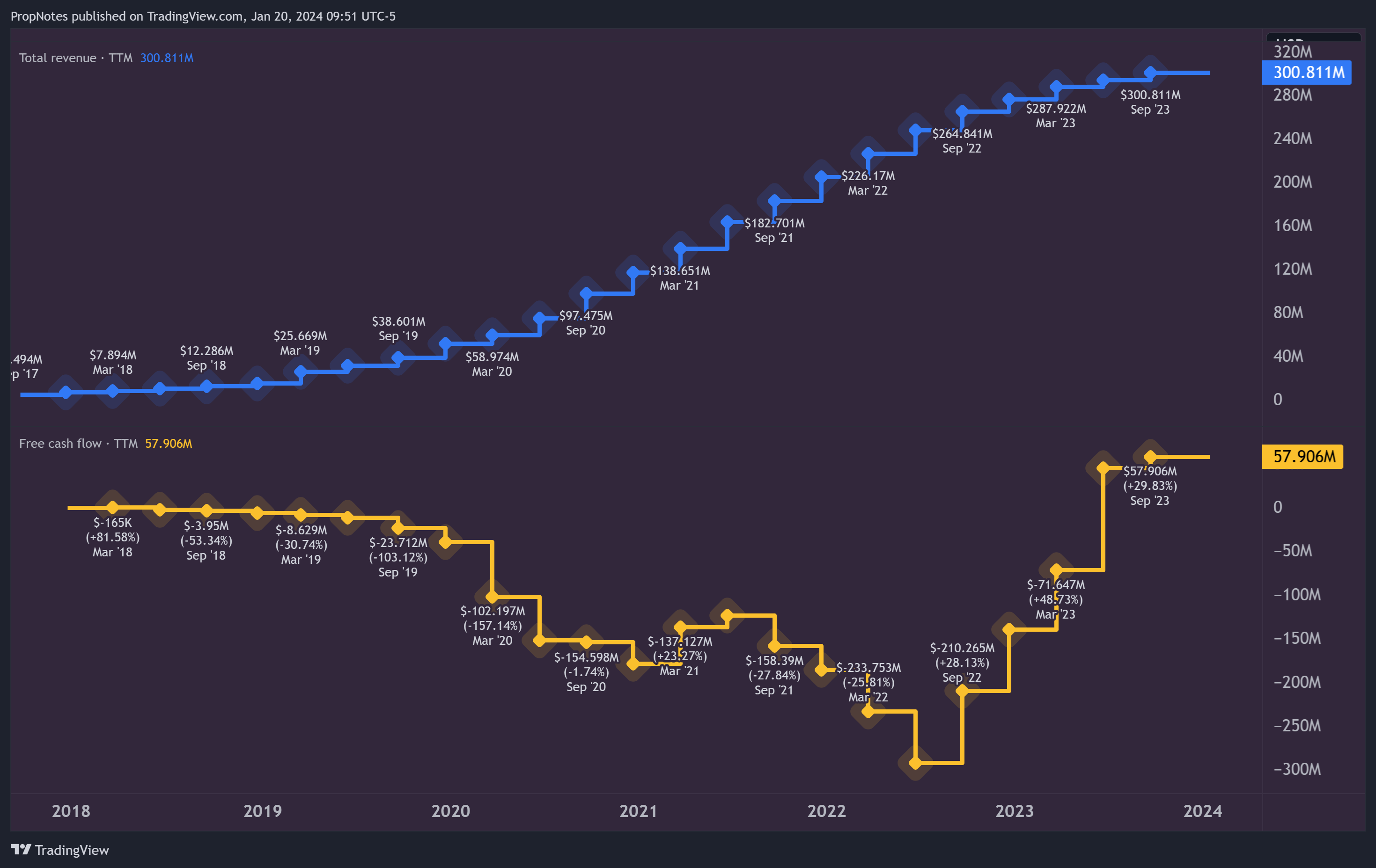

Zooming out traditionally, this ‘healing’ narrative appears real when taking a look at the business’s leading line development and capital, with TTM FCF lastly in the black once again following a duration of difficulties:

TradingView

This likewise couple with a favorable market outlook. On a current revenues call, CEO Paul Smithers had the following to state:

I want to keep in mind that even throughout this macroeconomic environment, development of the total marijuana market in the U.S. continues to stay strong, with BDSA forecasting marijuana sales of $29.5 billion in 2023, representing roughly a 12% development from 2022. Furthermore, BDSA approximates that roughly 60% of U.S. grownups might have access to adult-use marijuana by 2026 with brand-new state programs coming online.

This does not always indicate that IIPR will see a lion’s share of this development offered its digressive position as a property owner, however it does supply a much better need environment for its centers gradually which includes stability to our viewpoint of IIPR’s future circulations.

Assessment

Rotating now to evaluation, if you take a look at the green chart above, you might be deceived into believing that IIPR is a good deal today, as the blue line is outlining a ‘reasonable worth’ of 30x FFO, and the orange line is outlining a reasonable worth (based upon historic FFO development) of 19x.

To us, an FFO numerous closer to ~ 12x appears better, thinking about that IIPR’s development moving forward is anticipated to be rather anemic. There is one only expert out there forecasting 2025 FFO of $13/ share, which to us appears high:

Quickly Charts

Nevertheless, if you outline a 12x FFO, then IIPR seems trading right around reasonable worth. This is likewise in line with the market, that makes sense offered the much slower development trajectory that’s been articulated by management and experts.

More broadly, IIPR does have a commonly varied portfolio of operations, consisting of a low level of concentration in any one client or any one state:

Our portfolio continues to be well diversified without any one occupant representing more than 16% of our annualized base lease and no state representing more than 15% of our annualized base lease.

When integrated with the beautiful balance sheet, we want to extend our reasonable worth FFO numerous quote variety to ~ 14x, which would put it at a small premium to the sector.

Management does anticipate that development will start to re-accelerate in the future which the existing downturn is because of the business placing itself to record that development.

Nevertheless, we’re less particular about the development outlook.

While market development ought to even more protect the dividend as we pointed out in the last area, as a REIT, IIPR preserves a loose relationship with the development of the controlled cannabis market.

This has actually been a relative favorable for the stock over the last couple years, as assessments and development for leading business like Canopy ( CGC) and Tilray ( TLRY) have actually subsided substantially.

Nevertheless, on the other side, IIPR ought to see less utilize to market development than manufacturers, as an insulated property play moving forward, if and when that happens.

So, it is difficult to see where precisely IIPR’s development will originate from moving on, and the business’s natural sale-leaseback program isn’t predicted to materially increase development either:

IIPR Site

The Dividend

So, where is the benefit here?

Currently sitting at ~ 8%, IIPR’s yield is the most appealing feature of the stock.

IIPR’s FFO development is slowing as the market absorbs a variety of continuous difficulties, and the stock itself (when priced on future development) seems trading at something estimating reasonable worth. Nevertheless, the dividend looks rather enticing.

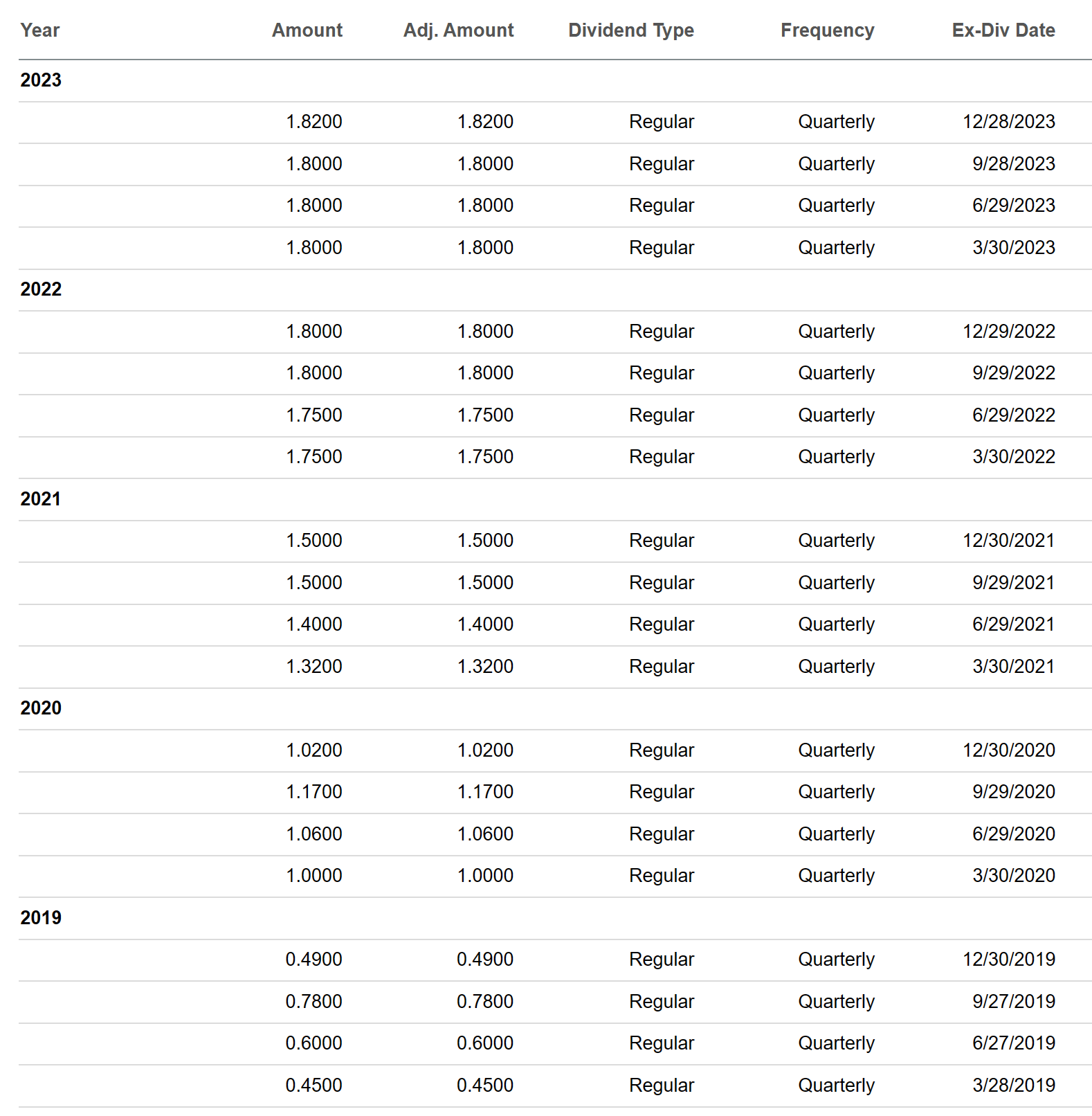

At present, IIPR pays about 79% of trend, which results in a yearly yield of 7.93% on a positive basis.

The business has actually grown this payment for 6 years now, from 2.32 per share in 2019, to $7.22 in FY 2023:

Looking For Alpha

This development has actually been very well constant and quick, however the genuine quality here comes when you have a look at the low level of total danger:

Looking For Alpha

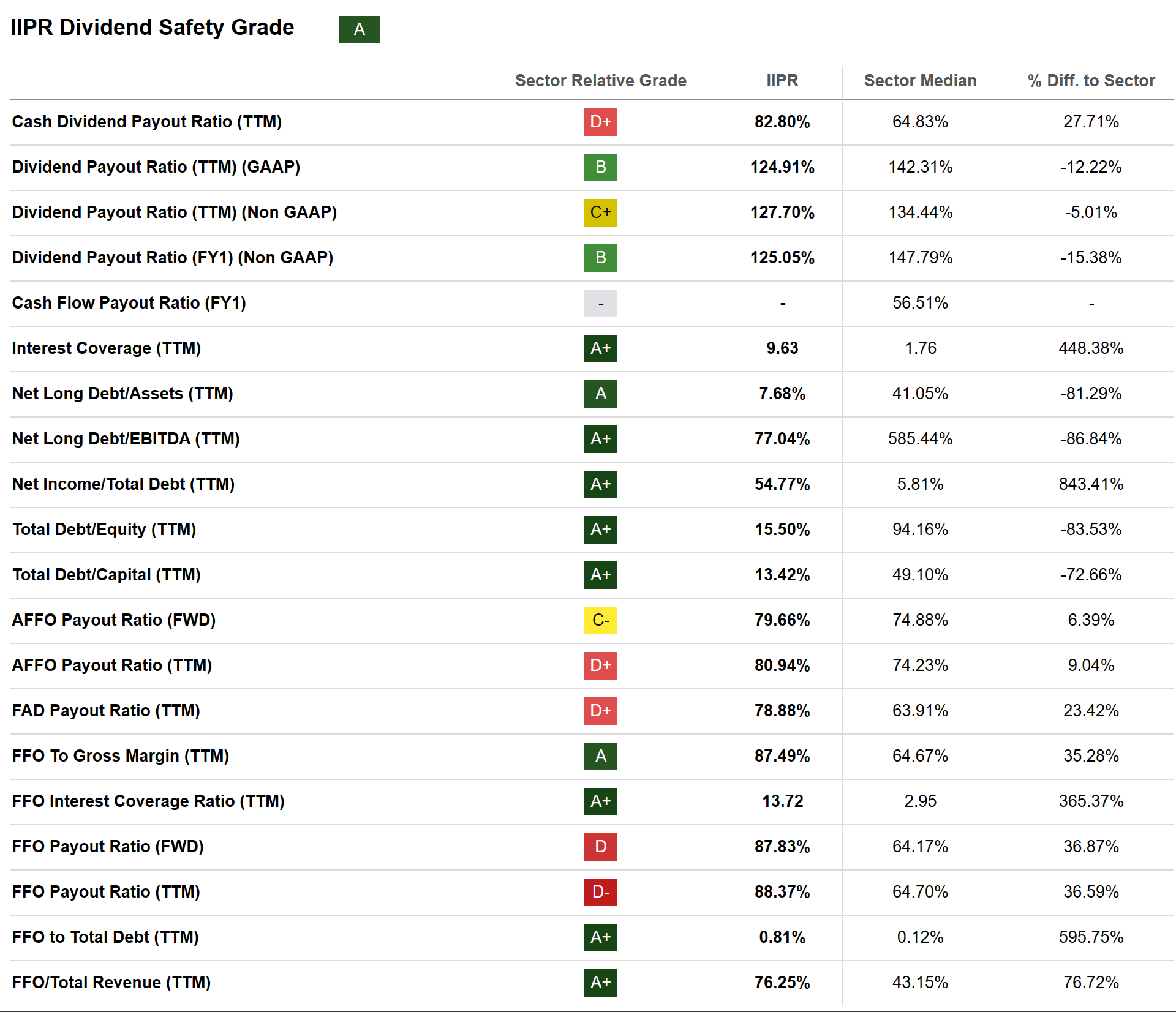

Looking for Alpha’s Quant Ranking System offers IIPR’s dividend security a grade of ‘A’, which is more than well-deserved when taking a look at a few of the ratios.

Amongst these metrics is an interest protection ratio of 9.6 (which is 4x greater than the sector), which shows that IIPR has a low level of interest commitments that might obstruct of the business’s future payments.

Furthermore, the business sports an extremely high FFO to Gross Margin portion, which shows that IIPR runs an extremely tight ship in regards to business expenses.

Lastly, IIPR’s Overall Financial obligation/ Capital (which we pointed out before) is really low, which shows that the business’s balance sheet is extremely healthy. This is among the primary threats when it pertains to buying REITs – the utilize. If REITs are too extremely indebted, then it can end up being an extremely dangerous proposal being an equity holder, as banks and shareholders will ultimately desire their refund, which can seriously constrain payments, or avoid them completely.

Therefore, in general, it would appear that the dividend is really safe. As far as development, it appears depending on IIPR’s FFO development as an entire, which, as gone over, ought to be fairly weak.

Dangers

There are a variety of threats to IIPR’s service, consisting of regulative concerns and matching threats to the business’s occupants. Here are a couple of methods this might manifest in truth:

- Marijuana market modifications: IIPR’s service is greatly dependent on the legal status of marijuana. Any modification in policies, consisting of restriction or increased constraints, might affect occupant need and rental earnings.

- Occupant compliance: IIPR rents residential or commercial properties to marijuana operators, a few of whom might deal with legal or compliance concerns in the future. This might result in defaults on lease, affecting IIPR’s monetary efficiency.

- Licensing hold-ups: Acquiring state licenses for marijuana growing and processing is a complex and lengthy procedure. Hold-ups in licensing for IIPR’s occupants might affect residential or commercial property tenancy and lease payments.

All of these might likewise affect IIPR’s numerous, which has actually differed a fair bit for many years. In the past, IIPR has actually balanced an FFO evaluation of ~ 30x, however if development flatlines or dips into the unfavorable, then our quote of 12-14x FFO might be too positive, and the business’s shares might be sold even more.

Lastly, the business reports revenues in about a month and will continue to do so into the future, which constantly triggers short-term volatility. For Q4 2023, we’re anticipating a decently more powerful quarter with a leading line development rate of 9.5% and minimal FFO enhancements. Nevertheless, if this modifications or the marketplace’s response to the numbers is bad, then the stock might drop.

Summary

In General, IIPR is a fascinating case due to its extremely robust existing operations however likewise weak development profile. Therefore, the shares themselves look relatively valued where they are, however the dividend appears strong and well covered.

For earnings candidates, it’s a fantastic choice.

For those looking for capital gratitude, looking somewhere else may be more ideal.

In general, we rank the stock a “Buy” due to its competitive Overall annualized ROR profile, although we acknowledge that the stock might not be for everybody.

Cheers!