Khanchit Khirisutchalual/iStock by means of Getty Images

By Marine Leleux, Sector Strategist, Financials

Why you ought to understand about NBFIs

Non-Bank Financial Intermediaries (NBFIs) have actually grown considerably considering that 2008 and as an outcome, the sector’s impact has actually come under increasing analysis. In 2015’s UK gilt crisis was another wake-up call for regulators, with issues increasing over the growing vulnerabilities. Regulators around the world are now requesting for more and more stringent policy of these activities.

In contrast to NBFIs, banks have actually seen more stringent policy considering that the worldwide monetary crisis, leaving space for NBFIs to establish. Nevertheless, in the face of the increasing intricacy and interconnectedness of the sector, an extreme shock to NBFIs might infect banks, developing a brand-new kind of threat for the standard banking sector.

NBFIs have numerous faces, consisting of ones that can appear like a bank

The term NBFI is utilized to explain a big range of organizations. We are categorizing them all as non-banks that take in money and utilize it to produce a return. The majority of NBFIs take in money, simply as banks do, and release it in numerous securities and derivatives. The Financial Stability Board (FSB) keeps track of NBFI activity and divides the sector in 2:

- NBFIs not taking part in credit intermediation nor bank-like activities (about 75% of the sector).

- All the entities which have bank-like activities, likewise called the “narrow step”, where Cash Market Funds and Fixed Earnings Funds comprise the biggest part (for other financial functions, see annex).

Another method of taking a look at NBFIs is just by dividing them into the primary elements such as:

- Insurance Coverage Corporations (ICS).

- Pension Funds (PFS).

- Other Banks (OFIs), such as Financial Investment Funds and Cash Market Funds

- Monetary Auxiliaries (FAs), such as insurance coverage brokers and captive banks.

Quick development made NBFIs much bigger than the banking sector

The more stringent capital and liquidity requirements on banks put in location after the worldwide monetary crisis – especially through the execution of Basel III – made some parts of providing less appealing for the banking sector. NBFIs were currently present prior to 2008 however actioned in to take control of parts of this organization as regulative requirements grew for banks. The IMF highlights that NBFIs have actually ended up being an important motorist of worldwide capital streams for emerging markets and establishing economies. Checking out the various NBFI elements and tasting 21 significant worldwide economies and the euro location (list of nations in the annexes), the FSB reported strong development for the sector in 2021, at 8.9% year-on-year. This is a substantial advancement as the sector has actually seen typical development of simply 6.6% over the last 5 years.

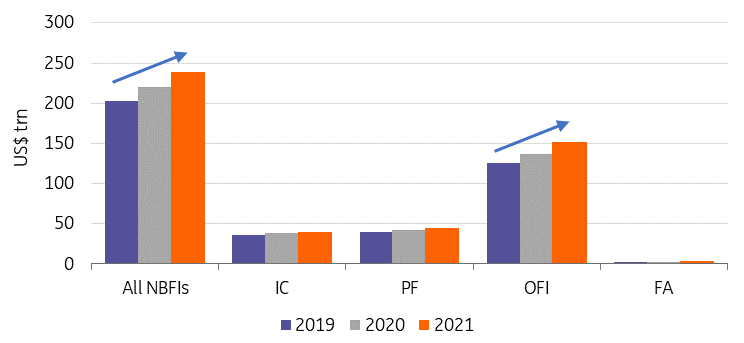

The NBFI sector has actually grown in every element considering that 2019 to reach $239.5 tn.

The element with the most essential development is OFIs.

FSB NBFI Keeping Track Of Report 2022, ING

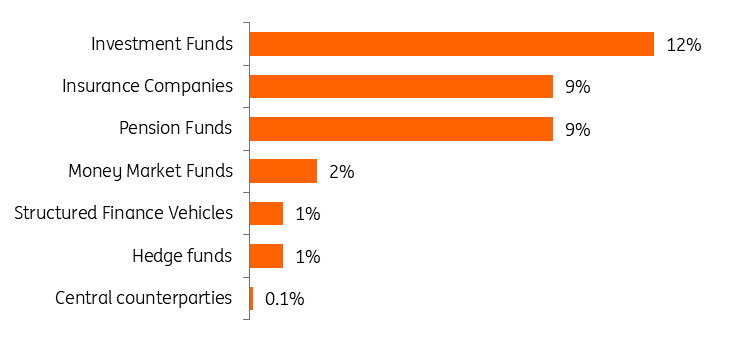

The IMF approximated the size of the sector in more information by taking a look at the particular share of the Global Financial Assets for each sub-sector of NBFIs.

Mutual fund are the most essential NBFI sub-sector representing 12% of worldwide monetary properties

Insurer and pension funds follow, at 9% of the worldwide monetary properties.

IMF Financial Stability Report 2023, ING

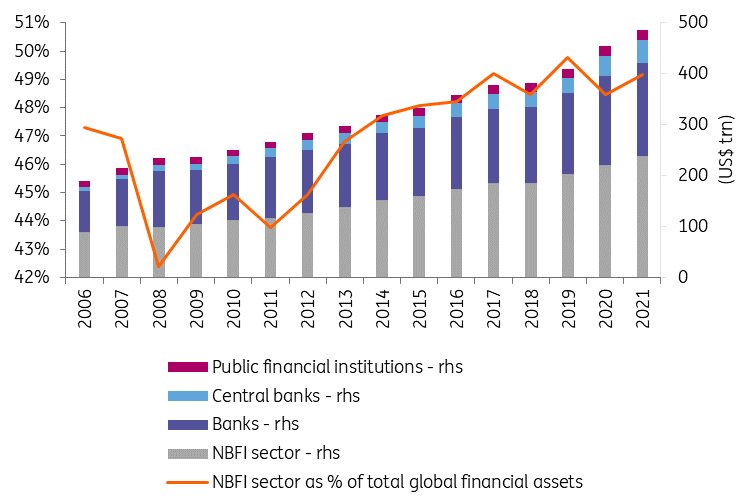

In General, these organizations now represent a 49.2% share of overall worldwide monetary properties, going beyond banks at 37.6%. The remainder of the market is made up of reserve banks and Public Financial Institutions.

The NBFI sector has more than doubled considering that 2008

In 2021, it reached 49.2% of overall worldwide monetary properties with banks representing 37.6%.

FSB NBFI Keeping Track Of Report 2022, ING

NBFIs represent 63% of nationwide monetary properties in the United States. In the eurozone, the sector is less substantial though it has actually still doubled in size considering that the worldwide monetary crisis.

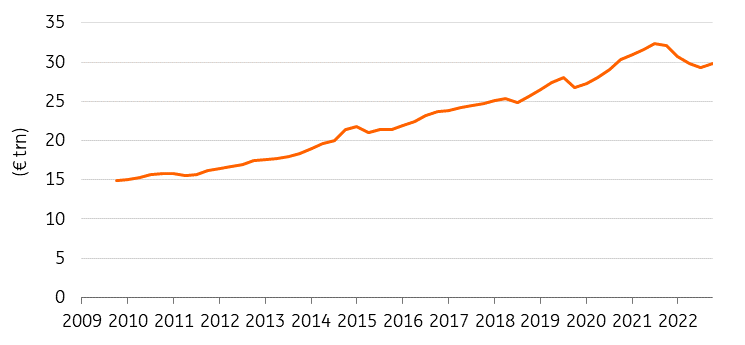

Overall NBFI properties in the euro location have actually doubled considering that 2009

Euro location NBFI properties lessened in 2022 as the sector offered higher-risk properties gotten throughout the low rates of interest duration.

ECB information, ING

Relative to the banking sector, NBFIs stay lesser: The European Reserve bank kept in mind that the sector had actually reached about 80% of the size of the banking sector in the eurozone in 2022. This is substantial however stays much smaller sized when thinking about the size of the sector internationally.

In both locations, the sector has actually established considerably after taking a struck throughout the worldwide monetary crisis, gaining from the more stringent guidelines on banks and the look for greater returns. In its 2023 monetary stability report, the IMF highlighted that the previous low rates of interest environment had actually triggered NBFIs to move their financial investments to riskier properties in the hope of discovering greater returns. However with increasing yields and an aggravating outlook for credit threat, NBFIs have actually begun to offer their riskier properties. With this advancement comes current issues over increasing NBFI vulnerabilities.

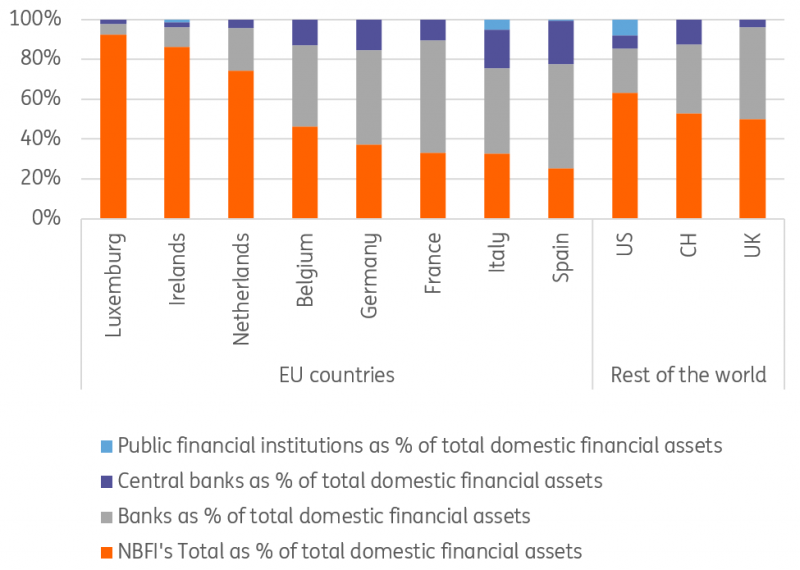

The share of both banks and non-banks in relation to overall domestic monetary properties varies considerably in between nations.

Luxemburg, Ireland and the Netherlands have really essential NBFI sectors, the very first 2 since they host numerous mutual fund as the latter has a big pension fund sector. On the other hand, in France and Spain, overall domestic monetary properties stay primarily controlled by standard banks. Variations in the NBFI sector size and type in between Europe and the rest of the world, and likewise in between European nations, show that Europe is not similarly exposed to the NBFI sector’s vulnerabilities.

NBFI share of overall domestic monetary properties differs considerably in between nations

In Europe, the share of NBFIs of overall domestic monetary properties is the greatest in Luxemburg

FSB NBFI Keeping Track Of Report 2022, ING

The sector is dealing with 3 primary vulnerabilities

Non-Bank Financial Intermediaries were thrust into the spotlight as soon as again this year following the current chaos in the banking sector. The primary issues develop from the lighter guidelines and following absence of information and evaluation of their threat direct exposure. While it stays tough to plainly evaluate the sector’s precise direct exposures, worldwide organizations recognize 3 primary threat aspects stemming from the present state of the sector particularly: monetary utilize, liquidity threat, and interconnectedness.

1. High monetary utilize in times of lower rates of interest

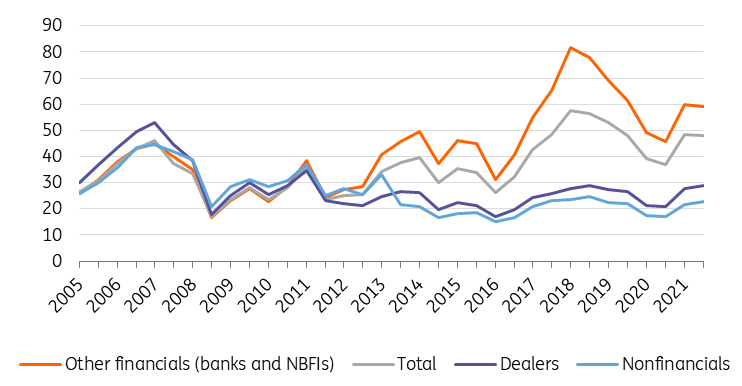

Low rates of interest in the last few years and possession rate volatility incentivised financiers to utilize utilize to enhance returns. Nevertheless, the level of vulnerability from leveraging has actually shown to be tough to approximate both for authorities and market individuals. The substantial absence of information makes a concrete evaluation of the threat challenging. Moreover, the IMF has actually worried that monetary utilize utilized by NBFIs can be found in numerous kinds, such as using repurchase arrangements, margin loaning in prime brokerage accounts, or artificial utilize related to using numerous monetary derivatives (like futures and swaps).

The current concentrate on using utilize originates from the increased threat of monetary distress due to the greater vulnerability to abrupt modifications in possession rates as rates of interest increase quickly. This might require NBFIs to de-lever, magnifying the preliminary rate decrease, with the gilt crisis being a case in point. The chart listed below from the IMF highlights well the current boost in using artificial utilize (where banks and NBFIs are lumped together), thus the growing vulnerability to abrupt rates of interest shocks.

The proxy for artificial utilize reveals a boost in utilize usage by banks and NBFIs considering that 2016.

Using utilize dropped in between 2018 and 2020 prior to increasing once again till 2021 and stabilising today

IMF Financial Stability Report 2023, ING

2. An absence of liquidity might worsen monetary market tension

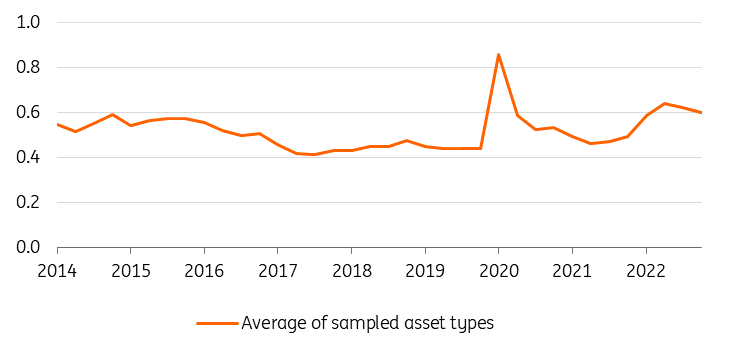

Liquidity dangers can can be found in various shapes and kinds. In its 2023 Financial Stability Report, the IMF highlights numerous kinds of NBFI vulnerabilities connected to liquidity.

NBFIs tend to have a liquidity inequality by holding reasonably illiquid properties while in some cases permitting financiers to redeem shares everyday This practice is not brand-new as pre-2008, shadow banks were currently using such an inequality. The current advancement in the sector highlights a boost in the liquidity inequality of the properties held by NBFIs. Checking out the vulnerability step recording weighted typical funds owning a possession and specifying liquidity as the portfolio-level bid-ask spread throughout funds, the following chart from the IMF plainly highlights this point. It reveals the spike in vulnerability to liquidity inequalities as Covid struck however likewise the more current boost. While not as substantial as the spike seen throughout the pandemic, current patterns are a suggestion that the sector is still susceptible to modifications in liquidity, which can typically aggravate in times of tension.

Typical liquidity inequality has actually increased considering that the Covid crisis

The liquidity inequality index, which surged in 2020 and once again over 2022, is now revealing a decrease

IMF Financial Stability Report 2023, ING

Moreover, the mix of monetary utilize and absence of market liquidity can cause a decrease in possession rates and a wear and tear of financing liquidity (liquidity spiral). For the majority of NBFIs, there is a threat that financiers withdraw funds, particularly when possession worths drop, although, for some, there might be notification durations to work out. For instance, hedge funds generally have a lockdown duration under which there can be no withdrawals. If enough required selling happens, it contributes to the pressure on the possession side, leading to something of a death spiral.

In 2022, the duration of tension in UK pension funds began with issues about the UK financial outlook triggering a sharp increase in gilt yields, which caused big mark-to-market losses on the fixed-income portfolio of defined-benefit pension funds. This triggered margin and security calls that pension and liability-driven mutual fund needed to satisfy through the sale of gilt securities, pressing gilt rates even lower. The Bank of England was required to reveal momentary and targeted purchases of long-dated gilts and index-linked gilts to stabilise rates. The objective of this intervention was to enable liability-driven mutual fund to rebalance without magnifying the preliminary shock. This episode reveals that, despite the fact that pension funds and insurer are not actually exposed to maturity improvement dangers (like other NBFIs are), they are still at threat of being captured in a death spiral. Moreover, other NBFIs would be exposed to the threat of financiers withdrawing which would even more enhance this threat.

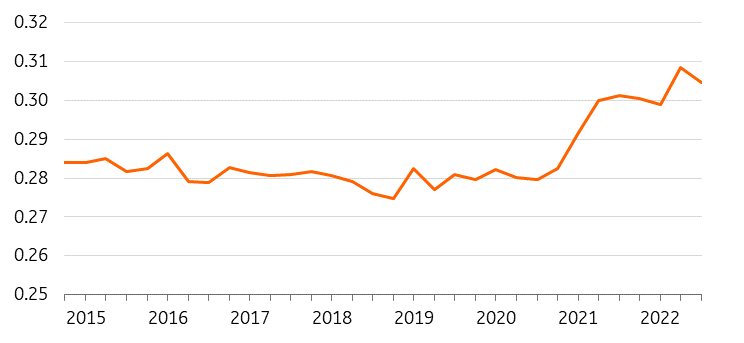

Furthermore, direct exposure to a focused portfolio of properties integrated with liquidity shocks can enhance tension occasions For instance, redemptions can require mutual fund to offer properties, depressing rates and resulting in additional sales by other market individuals with comparable portfolio holdings, therefore, magnifying the preliminary shock. Regrettably, over the last 2 years, mutual fund portfolios have actually ended up being significantly comparable, increasing the hazard of associated liquidity shocks. This is a lot more essential as NBFIs have actually likewise grown in size.

Increasing resemblance in NBFI portfolios’ possession class considering that 2020

IMF possession class resemblance index reached 0.3 points in 2022

IMF Financial Stability Report 2023, ING

3. Interconnectedness

NBFIs have actually grown in value considering that 2008, indicating that their function has actually increased in both domestic and cross-border capital circulations. They have actually likewise ended up being more interconnected with the remainder of the monetary system which considerably increases the intricacy of the sector. This might cause growing vulnerabilities and dangers and act as a shock amplifier. The interconnectedness has not just increased in between NBFIs and other banks like banks however likewise in between the various kinds of NBFIs.

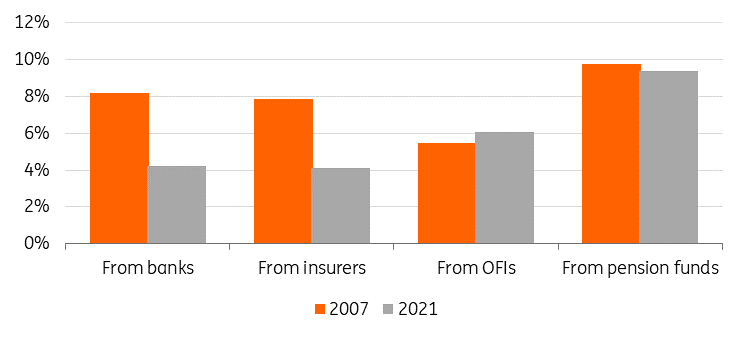

OFIs’ financing from banks visited 4 portion points as a portion of overall properties

Financing from pension funds stayed steady and increased from other OFIs

IMF Financial Stability Report 2023, ING

Bank linkages to NBFIs have actually nevertheless been increasing in time which can be described by the increasing size of the NBFI sector. With IMF information, we can see the boost in both claims and liabilities from banks to NBFIs.

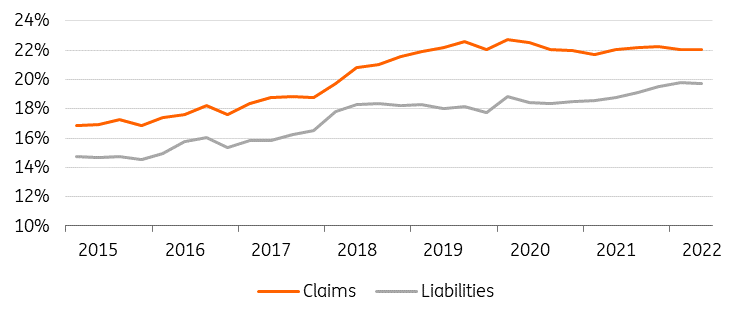

NBFIs now comprise about a fifth of banks’ properties and liabilities

Banks’ claims to NBFIs reached 22% of overall cross-border claims as liabilities are around 20% of overall cross-border liabilities.

IMF Financial Stability Report 2023, ING

Bank liabilities towards NBFIs (as a portion of overall cross-border liabilities) have actually increased by 5 portion points considering that 2015. The very same pattern shows up for claims to NBFIs which went from 17% to 22% in the seven-year duration.

When once again, the interconnectedness in between the standard banking market and the NBFI sector significantly differs in between nations. Information from the FSB permits us to examine banks’ direct exposures and usage of financing from various NBFIs in 2021 at a nationwide level (for the 29 nations chosen), revealing substantial distinctions.

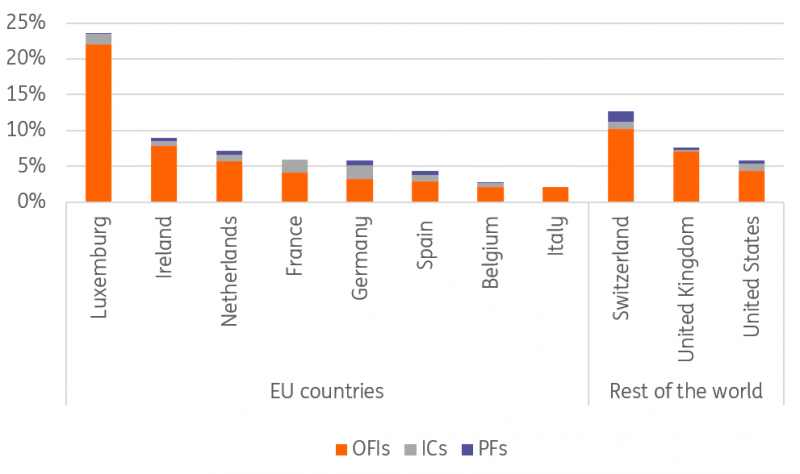

Crucial variations in banks’ usage of financing from NBFIs as a portion of overall bank properties in 2021

In Europe, Luxemburg is the front-runner with almost 25% of its overall bank properties moneyed by NBFIs

FSB NBFI Keeping Track Of Report 2022, ING

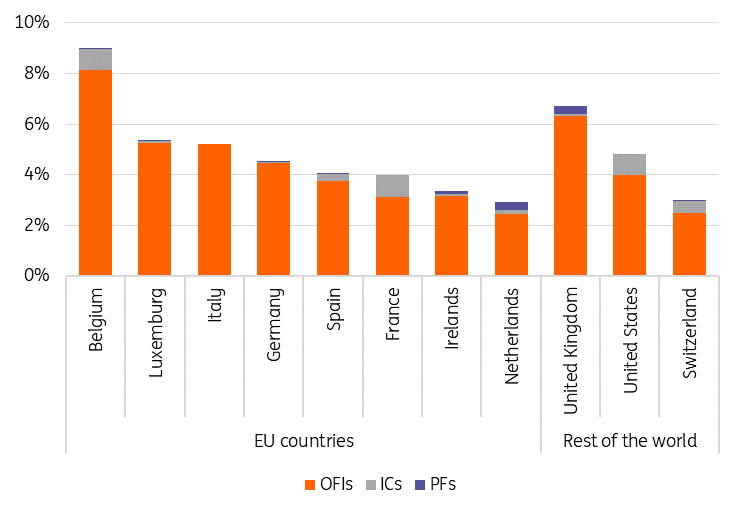

Crucial variation in banks’ direct exposure to NBFIs as a portion of overall bank properties in 2021

In the EU, Belgium is the most exposed to NBFIs, at 9% followed by the UK at almost 7%.

FSB NBFI Keeping Track Of Report 2022, ING

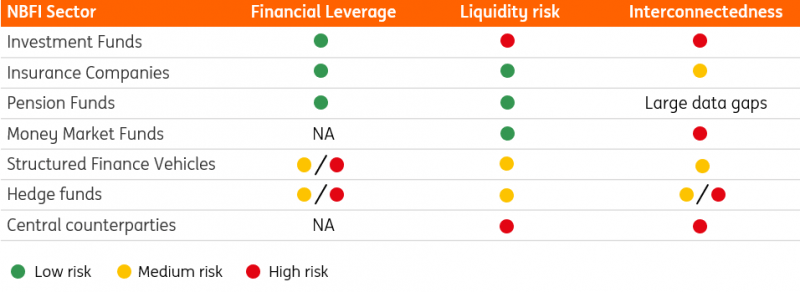

The value of these 3 primary threat classifications likewise differs depending upon the NBFI sub-sector. The following table from the IMF approximates the monetary utilize, liquidity, and interconnectedness dangers for each NBFI sub-sector.

Mutual fund are dealing with high vulnerability to liquidity and interconnectedness dangers

As the biggest sub-sector, mutual fund’ high-risk ratings would indicate a substantial effect on the sector in case of a significant shock.

IMF Financial Stability Report 2023, ING

Spillover threat to banks

The previous area took a look at the most popular dangers for the NBFI sector. Nevertheless, no information presently exists to make an estimate of the prospective effect on banks if these organizations were to see substantial tension occasions. However, we can recognize some direct and indirect channels through which tension on NBFIs would impact banks.

Direct effects

To start with, the majority of banks count on NBFIs for financing, as displayed in the previous charts. Tension in the sector may straight impact banks’ capability to money themselves, potentially resulting in a abrupt shock in financing expenses

Second of all, banks have direct exposure to these NBFIs, which might cause credit threat for banks Some discomfort on the possession side, nevertheless, would not bring the common NBFI down and the hit would primarily be taken by financiers in the funds.

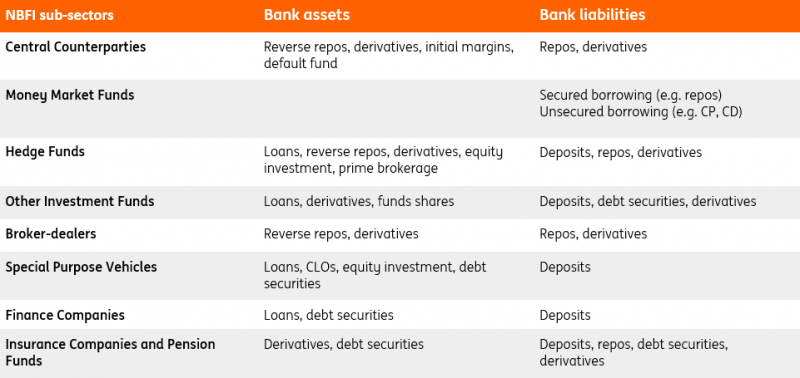

The Bank of International Settlements highlighted in the chart listed below, the various direct exposure that banks can need to NBFIs, and therefore the prospective direct effects. It likewise explains the strong interconnectedness and resulting absence of openness of both sectors.

Illustrative examples of properties and liabilities links in between banks and NBFIs

Bank of International Settlements, ING

Indirect effects

Most Importantly, both the direct and indirect results would accumulate as they would likely happen at the same time. We see 3 indirect effects that would happen in case of extreme tension on the NBFI sector.

1. Financial instability and possession worth drop

As discussed, shocks to NBFIs might cause fire sales of properties, which might itself cause chaos in monetary markets Banks would likewise be impacted by means of the drop in worth of a few of their properties.

Provided the bigger size of the NBFI sector, the results will be more powerful than in the past. This would injured the worth of the properties that banks utilize as security themselves (e.g., in liquidity operations with the reserve banks), therefore striking the capability of banks to money themselves. Likewise, this would strike the security that banks need from clients On the occasion that the resulting margin calls could not be fulfilled, this might cause credit losses for banks and potentially lead to doubts about the bank itself.

2. Wealth results in the population

Shocks to NBFIs would cause a hit to the worth of their financial investments. The majority of hedge fund financiers and other monetary intermediaries are thought about to be high-income people, who would experience an unfavorable wealth impact, leading them to invest less. However, this would not have a huge effect on the more comprehensive economy, as costs amongst high-wealth people really has a minimal relationship to their wealth. Nevertheless, this is not the case for pension funds. One might anticipate a shock impacting numerous pension funds or one fund, in specific, (as we have actually seen in the UK) toaffect the middle-income population. On top of being a big self-confidence shock, this might possibly affect the solvency and default likelihood of a part of banks’ middle-income clients. With a shock big enough, this might likewise indicate less costs and a possibly substantial downturn of the more comprehensive economy.

3. Credit accessibility and expenses, impacting the loan book

NBFIs play a crucial function in the economy by offering access to credit to those who can not obtain at a sensible expense through banks. An essential tension might imply a contraction in credit and abrupt greater funding expenses in the genuine economy. This would slow the economy down and for that reason likewise affect the banking sector.

Moreover, the link in between a customer and an NBFI (such as a mutual fund) is less strong than in between a bank and its customer. When the going gets hard, banks typically support their customers. Mutual fund might not have this very same reward. This might imply that banks will be taking a look at a scenario where either they see their customer defaulting (if the NBFIs do not extend their financing) or they are required to re-finance. These characteristics might push bank loan quality.

A monetary shock that strikes the NBFI sector might cause monetary tension in the banking system both by means of direct and indirect channels.

A banking crisis might likewise be gotten worse by the existence of NBFIs

We have actually taken a look at the impact of tension on the NBFI sector. Nevertheless, if there is tension in the banking sector, NBFIs might likewise worsen that tension, even if they are reasonably safe themselves. Throughout the banking crisis previously this year, inflows to United States cash market funds were at an all-time high. Part of this has actually associated with deposit outflows from United States banks. In the not likely, however possible, occasion of a flight from banks into cash market funds, this might put banks under extreme tension.

The biggest ‘understood unidentified’

As discussed previously, no information presently exists to enable us to make a clear evaluation of the effect on banks if NBFIs were to see substantial tension occasions. The trouble comes from the absence of information on the sector. Undoubtedly, despite the fact that the regulative requirements differ in between NBFI sub-sectors, there stays a basic absence of policy and information requirements. Without information providing a clear summary of NBFIs, one can just broadly approximate where the vulnerabilities stand: which are most likely primarily in the United States. We likewise understand the vulnerabilities (utilize, liquidity, and interconnectedness) in addition to the direct and indirect channels through which the threat may propagate to the standard banking sector. All in all, we see this as the biggest “understood unidentified” threat for the monetary system.

A long roadway ahead towards more policy

Significant banks such as the IMF and FSB and reserve banks are plainly knowledgeable about the NBFIs’ vulnerabilities and absence of openness. They have actually stressed the requirement for policy of NBFI activities and recommend, for instance, permitting particular NBFIs access to reserve bank liquidity in times of tension. Likewise, they see a strong requirement to bridge the present information spaces and incentivise NBFIs to use more stringent threat management. The ECB has likewise just recently asked for that banks put more effort into the policy and tracking of their NBFI counterparties, passing the ball back into the court of the banks. In any case, the execution of such policy in a global, growing, varied, and significantly intricate sector will take years.

The roadway ahead to a totally controlled market is still long. In the meantime, if the sector deals with extreme tension which overflows to banks, financial authorities may be required to action in. Reserve banks stay the backstop and might – potentially hesitantly – need to reduce the threat of a full-scale monetary crisis coming from the development of the Non-Bank Financial Intermediaries.

The paradox

So, if the going gets hard for Non-Bank Financial Intermediaries, the banking sector might be impacted by the shock wave.

After a years of bank policy that reduced banks’ threat profiles and decreased the vulnerability of the banking sector, monetary dangers in other parts of the system have actually grown, positioning an indirect threat to the banking sector and a possible factor for reserve banks to action in. It’s a paradoxical circumstance, both for banks that have actually seen this sector grow much faster than the banking sector itself, in addition to for regulators who were intending to have actually handled monetary stability. In attempting to reduce threat, the threat has actually been considerably intensified.

Annexes

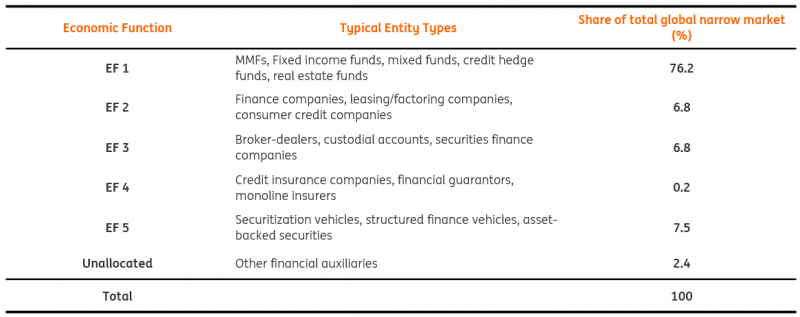

FSB category of narrow NBFI and particular share of the worldwide market (end of 2021)

FSB NBFI Keeping Track Of Report 2022, ING

List of nations consisted of in the 21 + euro location group

FSB NBFI Tracking Report 2022, ING

Material Disclaimer

This publication has actually been prepared by ING entirely for details functions regardless of a specific user’s ways, monetary circumstance or financial investment goals. The details does not make up financial investment suggestion, and nor is it financial investment, legal or tax recommendations or a deal or solicitation to acquire or offer any monetary instrument. Learn More

Editor’s Note: The summary bullets for this short article were picked by Looking for Alpha editors.